What Is Front Running in Trading? Definition, Examples & Legality

Picture this: a currency trader at a major bank gets a call. A corporate client needs to convert $3.5 billion into British pounds. A transaction that size will move the market, the trader knows it, the whole desk knows it. Instead of executing the client’s order, they quietly start buying GBP for the bank’s proprietary accounts. The pound moves up. Then the client’s trade goes through at the higher price. The client overpays by millions. The trader pockets the difference.

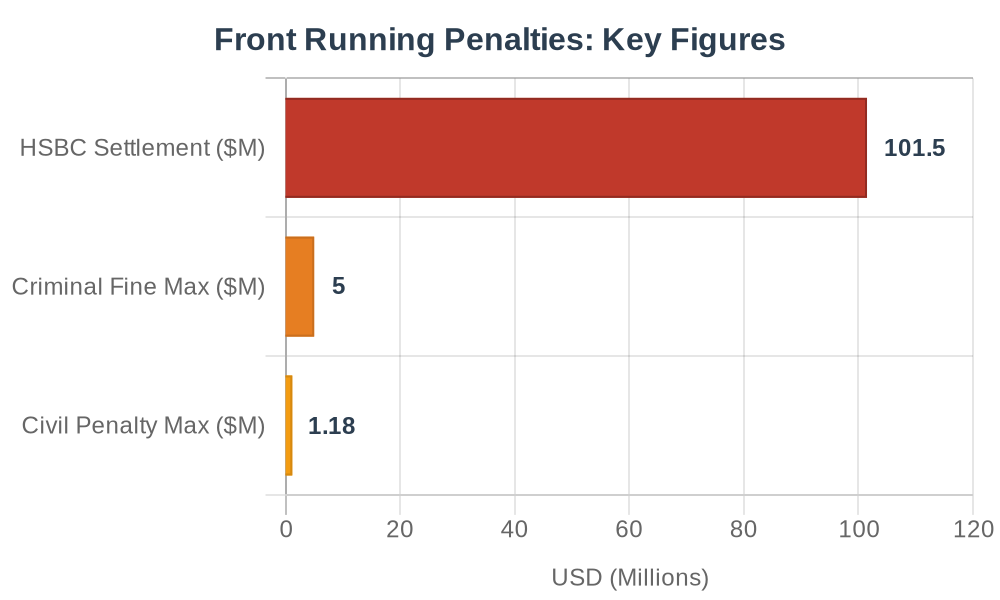

That happened. In 2011. At HSBC. The DOJ secured a federal jury conviction against the trader in 2017 and a $101.5 million corporate settlement with the bank in 2018; though the individual conviction would later be voided on appeal in 2022 after a related Supreme Court ruling narrowed the fraud theory underlying it.

To answer ‘what is Front Running’: It is one of those market abuses that sounds too calculated to be accidental. Someone entrusted with your order uses that information against you. It’s market manipulation, a breach of fiduciary duty, and in most forms, a federal crime.

Front running is the illegal practice of trading ahead of a known client order, exploiting non-public information about an imminent transaction to profit at the client’s expense. HSBC paid $101.5 million to the DOJ in 2018 after traders front-ran a client’s $3.5 billion FX transaction (US DOJ, 2018); the individual trader’s 2017 conviction was later voided on appeal in 2022. Under FINRA Rule 5270, trading ahead of a block transaction (10,000+ shares) is prohibited, with criminal penalties reaching $5 million and up to 20 years in prison.

What Is Front Running?

Front running is when a trader or broker executes orders in a security for their own account, or a related party’s account, before filling a known, pending client order. The edge isn’t market insight. It’s knowledge that a large order is about to move the price.

The legal concept turns on material, non-public information about an imminent trade. Not information about a company’s earnings or a pending merger, information about the fact that a specific, large transaction is coming. A broker who knows a pension fund is about to buy 500,000 shares of Company X isn’t smarter than the market. They’re just first. That’s the core of what makes it manipulation rather than sharp trading.

FINRA Rule 5270 defines the prohibited conduct precisely: no member may trade ahead of a block transaction in a security, or a related financial instrument, when they hold material, non-public market information about that imminent transaction (FINRA Rule 5270, 2013). Block transaction in equity markets means 10,000 shares or more. For smaller transactions, similar conduct can still violate FINRA Rule 2010 and Rule 5320.

The trust violation is what makes this different from other forms of market opportunism. The client shared the order because they needed execution services. That relationship is the breach.

How Does Front Running Work?

The mechanics are straightforward. Whether the market is equities, FX, or futures, the sequence rarely varies.

- A client typically an institution, not a retail trader, submits a large buy order. Large enough that the market will feel it when it executes.

- The broker’s desk now holds two things: the obligation to execute that order, and the knowledge of what executing it will do to the price. If they buy the security first, the client’s own order will drive the price up after them. That’s the setup.

- They trade ahead. Using the client’s non-public order information, the broker enters a position before routing the client’s order to market. This can happen in seconds on electronic systems.

- The client’s order executes at the now-higher price. The broker unwinds their position into that price movement. The profit is the spread between what the broker paid and what the market moved to after the client trade. The client effectively funded both sides of the broker’s trade.

The first time someone explained the mechanics to me, sitting in a coffee shop with a former FX trader; I assumed there had to be some friction in the system that prevented this. There isn’t. On modern electronic platforms, the gap between seeing a client order and routing a personal trade ahead of it is measured in milliseconds. The reason it doesn’t happen constantly isn’t technical difficulty. It’s surveillance and the fear of getting caught.

Front running doesn’t require the front runner to be the client’s direct broker. Market makers who receive order flow, prop trading desks within the same firm, or even traders who intercept information through information barrier failures can all participate. That’s why information barrier (Chinese wall) policies exist, to prevent trading desks from accessing order desk data in the first place.

Real-World Front Running Examples

The HSBC FX Case (2011/2018)

This is the benchmark case, though one with a complicated legal afterlife worth understanding in full. HSBC’s currency desk, led by then-head of FX cash trading Mark Johnson, received a client instruction (from Cairn Energy) to convert approximately $3.5 billion USD into British pounds sterling — one transaction, specific timing, massive notional size.

Johnson and his team bought GBP for HSBC’s proprietary accounts before executing the client’s trade. The purchase moved the pound. The client then bought at the inflated rate, paying tens of millions more than they should have. Johnson sold into that price move.

In October 2017, a US jury in Brooklyn convicted Johnson on one count of wire fraud conspiracy and eight counts of wire fraud. He was sentenced to 24 months in prison and a $300,000 fine. HSBC separately entered a deferred prosecution agreement with the DOJ in 2018 and paid $101.5 million — $63.1 million in fines and $38.4 million in restitution (US DOJ, 2018).

The case took an unusual turn on appeal. In 2022, the 2nd US Circuit Court of Appeals in Manhattan voided Johnson’s conviction in a 3-0 decision, ruling that the conviction was tainted because the Supreme Court had subsequently repudiated the “right-to-control” fraud theory underlying it in an unrelated case (Ciminelli v. United States). The appellate court also expressed “grave doubt” that an alternative fraud theory would have supported the conviction.

Despite the reversal, the HSBC case remains the defining real-world example of FX front running. The corporate settlement stands. The conduct was unambiguous on its facts. What changed was the legal theory available to prosecutors — not the underlying market abuse — and US enforcement agencies have since adapted their fraud charging strategies in similar cases. The case showed the FX market, which had long operated on informal norms, wasn’t exempt from securities enforcement.

A Standard Brokerage Example

Smaller scale, same structure. A broker receives a large institutional buy order for a mid-cap stock. Before routing it to the exchange, a trader on the desk buys 50,000 shares in a personal account. The institutional order clears, pushes the stock up 1.8%. The trader sells. That’s FINRA Rule 5270. It’s also a straightforward SEC enforcement case.

Index Front Running: The Legal Exception

Not everything that looks like front running is illegal. When S&P announces a stock will be added to the S&P 500, that information is public. Index funds tracking the benchmark must buy the stock before inclusion. Other participants who anticipate that forced buying and trade ahead of it are technically running ahead of a predictable order — but they’re acting on a public announcement, not a client’s confidential trade.

Thatdistinction is the entire legal dividing line. Winton Capital Management research estimated index front running costs passive investors at least 0.2 percentage points annually (Winton Capital Management, per academic citations). Legal, but not free — the cost is real, it’s just being extracted by market participants acting on public information rather than privileged client data.

Is Front Running Illegal?

Yes — with the index exception above.

Under US law, front running based on non-public client order information violates FINRA Rule 5270 for block transactions, Section 10(b) of the Securities Exchange Act and Rule 10b-5 for fraud and manipulation, and the CFTC’s analogous rules for commodity markets. The DOJ can prosecute it as wire fraud, as the HSBC case demonstrated.

UK traders face the Financial Conduct Authority’s jurisdiction under the Market Abuse Regulation (MAR). EU markets operate under ESMA’s parallel framework. The prohibition is consistent across major financial centres — using a client’s pending order as the basis for trading your own account is illegal.

The exception, index front running, holds because the legal principle is about the source of the information, not the action itself. Trading ahead of a predictable event based on public announcements doesn’t breach confidentiality. Trading ahead of a specific client order you were entrusted with does.

Understanding why insider trading is illegal covers the same legal reasoning — the prohibition exists to protect market integrity and the trust relationship between professional intermediaries and their clients.

Front Running vs. Insider Trading

Easy to conflate. Different at the root.

- Front running exploits information about order flow. The trade you’re running ahead of is large enough to move the market. The information advantage is purely mechanical — you know that buying pressure is coming and you position ahead of it.

- Insider trading exploits information about a company’s fundamentals. Unannounced earnings, a pending acquisition, a regulatory decision. The edge is about what the security is worth, not what the market is about to do.

In practice, they can overlap. A trader who front-runs an order in a stock that’s about to be acquired has potentially violated both rules simultaneously. Both involve a breach of fiduciary duty. Both involve material non-public information. The source just differs.

| Front Running | Insider Trading | |

|---|---|---|

| Information source | Client order flow | Company fundamentals |

| Who typically holds it | Broker, market maker, desk trader | Corporate insiders, tippers |

| Core violation | Misuse of client order data | Trading on material non-public corporate information |

| Legal framework | FINRA Rule 5270, SEC 10b-5 | SEC Rule 10b-5, Section 16 |

| Criminal exposure | Yes | Yes |

The Nancy Pelosi insider trading debate illustrates how allegations of trading on non-public information — even without conviction — generate significant public and regulatory scrutiny. Front running operates under the same spotlight, with the additional complication of an explicit client betrayal at its core.

A fuller breakdown of insider trading covers the legal framework in more detail.

The Penalties for Front Running

They’re significant. Prosecutors and regulators have shown they will use them.

Mark Johnson, the HSBC trader convicted in 2017, served a two-year prison sentence before the 2nd Circuit voided his conviction on appeal in 2022. The reversal turned on a narrow legal theory, not a finding that the conduct was acceptable. At the federal criminal level, individuals can still face fines up to $5 million and imprisonment up to 20 years per violation under US securities law, with prosecutors now relying on alternative fraud theories that survived the Supreme Court’s subsequent rulings.

Civil penalties run on top of that. The SEC’s 2025 adjusted civil penalty schedule sets maximum fines at $1,182,251 per violation where substantial gains or losses were involved — and disgorgement of all profits from the scheme is standard practice. Courts have shown no reluctance to stack criminal and civil penalties simultaneously.

Firms don’t escape. HSBC’s deferred prosecution agreement required independent compliance monitoring on top of the $101.5 million payment. In May 2024, Indian regulators arrested Axis Mutual Fund’s chief dealer Viresh Joshi in connection with alleged front-running trades exceeding ₹200 crore — roughly $24 million USD — with the Enforcement Directorate later freezing ₹17.4 crore in assets (SEBI, 2024).

The pattern across enforcement actions: the profit made from front running consistently ends up as the floor for disgorgement, with fines and penalties layered on top. Trading ahead of client orders is never, in practice, worth it.

How Do Regulators Detect Front Running?

Surveillance technology has improved the detection odds considerably.

FINRA and the SEC operate automated market surveillance systems that flag accounts trading ahead of large block executions, accounts that consistently profit just before significant price moves that follow client order completions. Pattern recognition at that scale used to require manual analysis. It doesn’t anymore.

The Consolidated Audit Trail (CAT), fully operational since 2024, records every US equity and options order with a complete timestamp trail, from origination at the broker through every routing step to final execution. Correlation analysis across the CAT data makes timing anomalies straightforward to identify. A trader who consistently buys 30 seconds before large client orders clear shows up in that data.

I’ve spoken with compliance officers at mid-tier brokerages who describe the CAT’s impact as a step-change. Before full implementation, proving timing correlation between a trader’s personal account and client order flow required weeks of manual reconciliation. Now it’s a query. The deterrent effect alone has changed behaviour on trading desks in ways that regulatory pronouncements never did.

The SEC’s whistleblower program also plays a role. Tips from insiders, colleagues, former employees, compliance personnel, trigger many enforcement investigations. The program pays 10–30% of sanctions above $1 million to qualifying tipsters (SEC Whistleblower Program). In the HSBC case, internal communications, specifically, the trader’s own statements to colleagues on HSBC’s internal network describing the intent to front-run became critical evidence once regulators began pulling records. That those communications survived even after the eventual conviction reversal underscores how routinely modern enforcement now turns on captured digital correspondence.

What This Means for Retail Traders

You can’t commit front running, you don’t have access to institutional order flow. But the structure matters to you as a potential victim.

The clearest retail exposure: dealing-desk brokers who can see your pending orders before execution. If a broker takes the other side of your trades, standard in dealing-desk models, they have a structural incentive to trade against your positions. That’s not always illegal front running in the legal sense, but the conflict of interest operates on the same principle.

No-dealing-desk (NDD) models eliminate that conflict. Orders route directly to liquidity providers. The broker’s revenue doesn’t depend on your losses. That execution structure matters more than headline spread comparisons.

Understanding how banks trade forex explains the institutional order flow dynamics that create the information asymmetry front running exploits. Knowing how that system works makes it easier to evaluate which execution models genuinely protect you.

When choosing a broker, ask specifically: does the firm operate on an NDD model? Are client orders routed directly to liquidity providers? If answers are vague, that’s the answer. What is a Forex Broker breaks down execution models in detail.

The Bottom Line on Front Running

Front running is illegal market manipulation, and the legal boundary isn’t subtle. When the information advantage comes from a client’s pending order rather than public market analysis, prosecutors and regulators treat it as fraud. The HSBC case (even after the 2022 appellate reversal of the individual conviction), the Axis Mutual Fund arrest, and ongoing SEC enforcement through 2024 confirm this is active enforcement territory, not a legacy rule gathering dust. Where US case law has narrowed specific fraud theories, prosecutors have adapted; the conduct remains prosecutable under multiple overlapping frameworks.

For retail traders, the practical priority is broker selection. Execution models that route directly to liquidity providers remove the structural conflict. For anyone operating professionally in finance, the compliance obligation is explicit: FINRA Rule 5270 requires written supervisory procedures specifically designed to prevent front running. That’s not optional.

If you’re building your trading knowledge from the ground up, how to learn trading covers the foundational concepts, including how markets actually work and why market integrity rules exist in the first place.

Frequently Asked Questions

1. Is front running always illegal?

No — but most forms are. Index front running is the main exception. Traders who anticipate index rebalancing based on publicly announced changes aren’t exploiting privileged information. The illegal variety requires non-public knowledge of a specific client order that you were entrusted to execute. That trust relationship is what the law protects.

2. What’s the difference between front running and insider trading?

Front running exploits knowledge of an imminent client order, the edge is about market mechanics. Insider trading exploits non-public corporate information: earnings, M&A deals, regulatory approvals. Both are illegal, both involve material non-public information, and both breach fiduciary duty. The distinction is the source of the information, not the act of trading on it.

3. How do regulators detect front running?

Automated surveillance systems track accounts that consistently profit ahead of large block executions. The SEC’s Consolidated Audit Trail provides a full timestamp record of every US equity and options order from origination to execution — making correlation between personal account timing and client order flow straightforward to analyse. Internal whistleblowers, operating under the SEC’s 10–30% reward program, trigger many enforcement investigations.

4. What are the maximum criminal penalties for front running?

Under US federal securities law, individuals face fines up to $5 million and imprisonment up to 20 years per violation. Institutional penalties are uncapped in practice, HSBC’s single deferred prosecution agreement cost $101.5 million. Civil disgorgement of all scheme profits is required on top of fines. The 2022 appellate reversal of the individual HSBC conviction narrowed one specific fraud theory but did not narrow these statutory maximums or the prosecutorial path under alternative theories.

5. Can retail traders be victims of front running?

Yes. If a dealing-desk broker uses knowledge of your stop-loss orders or pending positions to trade ahead of your execution, that conduct can constitute front running. No-dealing-desk (NDD) brokers route orders directly to liquidity providers and don’t take the other side of client trades — eliminating the conflict structurally.