Which is the Best Forex Card in India for Travel & Studies?

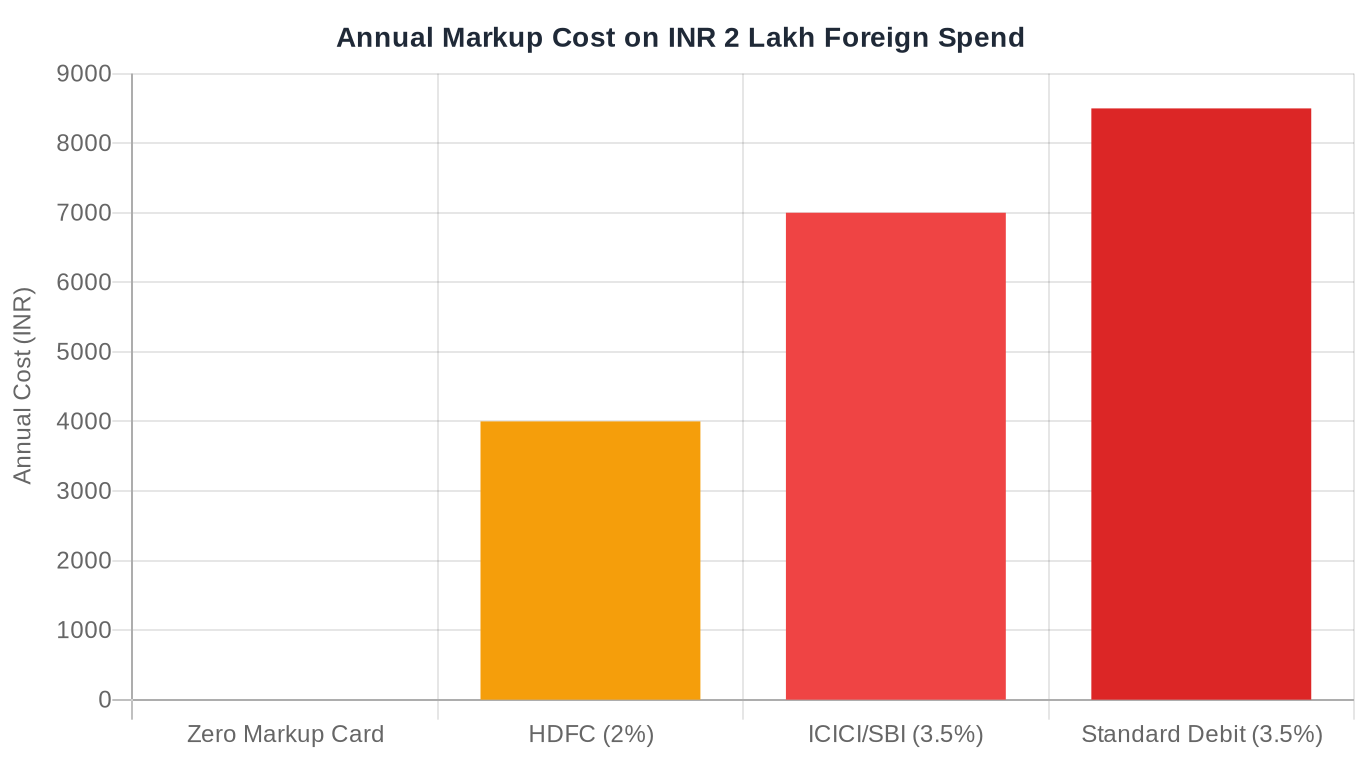

You land at Heathrow, tap your Indian debit card at the Tube machine, and think nothing of it. Until you check your bank statement three days later and realise you paid your bank a 3.5% markup on every single transaction. On a ₹2 lakh trip, that’s ₹7,000 handed over for no reason whatsoever. That’s a decent hotel night, gone.

Forex cards exist to stop exactly that. But not all of them do.

Some banks call their product “multi-currency”. Others advertise “zero markup” in the headline, then recover the margin through reload fees and ATM charges. Picking the wrong one doesn’t ruin a trip, but it adds up — especially if you travel more than once a year or you’re a student living abroad on a fixed remittance.

This guide cuts through the noise. Below are the best forex cards in India worth your attention in 2026, the ones to skip, and the math behind why the difference actually matters.

What Is a Forex Card?

A forex card is a prepaid card loaded with foreign currency before you travel. You load it in India at today’s exchange rate, then spend at your destination without worrying about daily rate fluctuations. No cross-border conversion fees on the loaded currency. No dynamic currency conversion traps. No surprise deductions on your bank statement when you return.

The underlying network is Visa or Mastercard on almost every card listed here, which means merchant acceptance is close to universal. Most cards support ATM withdrawals abroad as well. The card looks and works like a debit card — swipe, chip, or tap — and the amount debits from the preloaded balance.

The catch? Not all forex cards in India are created equal. “Multi-currency” covers everything from genuinely zero-fee products to offerings that quietly charge you on every reload, every ATM visit, and every currency you didn’t load in advance. The next section shows you what to interrogate before you apply.

What Should You Look for in the Best Forex Card for Indian Travellers?

Five things matter. Everything else is marketing copy.

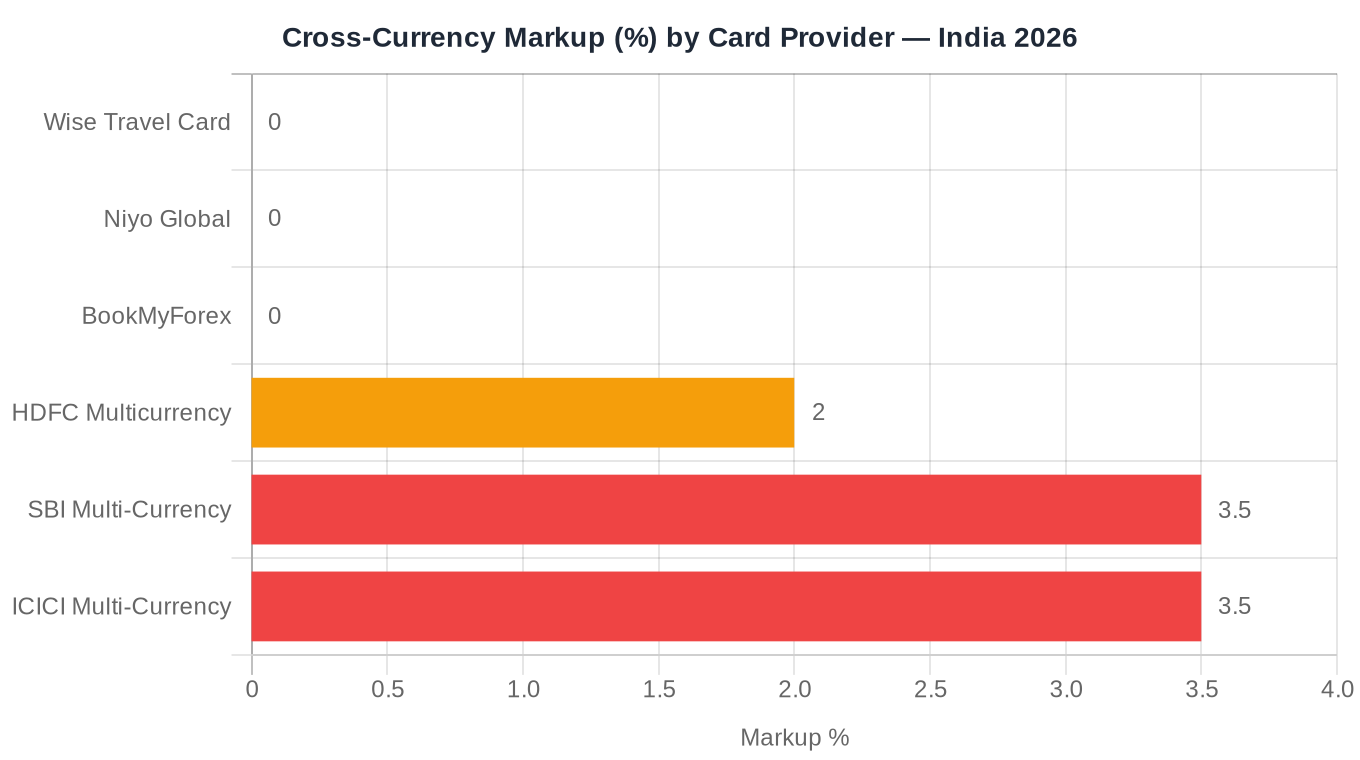

- Exchange rate markup is the biggest lever. A 3.5% conversion fee means ₹35 in silent fees on every ₹1,000 you spend. Over a ₹2 lakh international trip, that’s ₹7,000 extracted without a single visible charge. Cards like Wise, Niyo Global, and BookMyForex charge zero markup on the loaded currency — you spend at the rate you loaded, full stop.

“Banks still hide their markups and refuse to be transparent, because they believe hiding fees gets customers to overpay. They may be right. Not all people and business owners have the time and desire to calculate the hidden margins they are charged.” — Kristo Käärmann, CEO and Co-founder of Wise

- Reload fees are sneaky. Some cards advertise zero issuance but charge ₹75–150 per reload. If you top up four times before a long trip or top up mid-travel, those charges accumulate into something meaningful.

- ATM withdrawal fees matter if you travel to cash-heavy destinations — Southeast Asia, rural Europe, most of East Africa. HDFC’s Multicurrency card charges $2 per international ATM withdrawal. Wise includes two free ATM withdrawals monthly up to a threshold (roughly ₹11,500 equivalent each), then 1.75% beyond that. Know this before you land somewhere with a ₹10 minimum withdrawal option.

- Currency coverage becomes relevant on multi-destination trips. Niyo Global supports 130+ currencies. HDFC Multicurrency supports 22. Thomas Cook Borderless supports 12. If your route hits three or four countries, coverage breadth genuinely matters — cards that don’t support a currency charge you cross-currency conversion fees, which is the exact problem you were trying to avoid.

- Digital usability rounds it out. Can you reload at 11pm the night before your flight? Does the app show real-time balances in the local currency you’re spending? Cards from Wise and Niyo have a genuine operational edge over traditional bank-issued forex cards whose app experience hasn’t been updated since 2019.

The Best Forex Cards in India for 2026

Wise Travel Card: Best for Zero Markup and Global Coverage

Wise operates at the mid-market exchange rate, the same rate you see on Google. No markup. Zero fees on the loaded currency. For travellers who want the cleanest deal on exchange rates in 2026, this is where the market currently sits.

TheWise Travel Card supports 40+ currencies on a single card. ATM withdrawals are free twice a month up to a threshold; after that, a 1.75% fee applies. Card issuance is a one-time cost with no annual maintenance fee.

What Wise does well: transparent pricing, real-time app, instant top-ups via UPI and NEFT, virtual card for online spending before the physical card arrives. What it doesn’t offer: the travel insurance some traditional bank cards bundle in, or the network of physical branches that cautious travellers still want. Wise operates as a regulated e-money institution rather than a scheduled Indian bank — worth knowing if you need RBI-compliant LRS documentation for amounts above certain thresholds.

I’ve used a Wise card across three continents over the last two years. The single most useful feature isn’t the zero markup — it’s seeing the exact rate I’ll get before I tap. That visibility changes how you plan day-to-day spending in a way the marketing copy doesn’t capture.

Niyo Global: Best for 130+ Currency Coverage

Niyo partners with DCB Bank and SBM Bank to issue its Global card. The DCB variant carries a ₹499 + GST annual fee, waived when your average monthly balance hits ₹5,000. The SBM variant waives the annual fee entirely but requires opening an SBM bank account first.

Zero forex markup on all transactions. Zero reload fees. The Niyo app shows real-time balances and rate calculations before you spend, which proves useful mid-trip when you’re deciding whether to load more SGD or just pay the cross-rate.

130+ currencies covered is the best breadth among Indian-issued forex cards in 2026. Most competitors top out at 12–22 major currencies and hit cross-conversion fees on everything outside that list. If your travel is multi-destination or unpredictable, Niyo’s breadth is a genuine differentiator.

The trade-off: Niyo requires opening a DCB or SBM bank account, which adds a step. Not difficult, but it’s not a same-day process.

I tested Niyo specifically on a multi-country Southeast Asia trip, SGD in Singapore, THB in Thailand, IDR in Bali. The card handled all three without the cross-currency hit my old HDFC card would have charged. For trips with more than two destinations, the 130-currency breadth genuinely earns its place.

BookMyForex True Zero Markup Card: Best for No-Fee Travellers

BookMyForex is the purist’s option. Zero issuance fee. Zero reload fee. Zero ATM withdrawal fee. Zero cross-currency markup. That’s four zeroes on a product where every competitor charges on at least two of those four dimensions.

The BookMyForex card operates on the Mastercard network through a partnership with Transcorp. Currency coverage handles 30+ major travel destinations effectively, less broad than Niyo’s 130+ but sufficient for the US, UK, Europe, Australia, Southeast Asia, and the Middle East. The exchange rate is set at the time of purchase or reload using live interbank rates.

One honest caveat: the app experience is functional, not polished. If you’re coming from Wise or Niyo where product UX is a priority, BookMyForex’s platform feels more transactional. It does the job cleanly; it doesn’t try to be beautiful doing it.

The best-value forex card in India on a pure fee basis. If you load the right currencies before travel and don’t need exotic coverage, this is the cost leader.

HDFC Multicurrency Platinum ForexPlus Chip Card: Best for HDFC Account Holders

HDFC’s flagship forex product supports 22 currencies. Issuance fee: ₹500 + GST. Reload fee: ₹75 + GST per reload. Cross-currency conversion fee: 2%. ATM withdrawals abroad: $2 per transaction.

Those fees add up compared to the zero-fee cards above. On a ₹2 lakh annual forex spend, the 2% cross-currency charge alone costs ₹4,000. That said, HDFC has the infrastructure advantage, branch network across India, robust customer support lines, and relationship banking, that carries weight for risk-averse travellers who want a human to call if something goes wrong at 2am in Frankfurt.

The card integrates with HDFC NetBanking for reloads and blocks. Existing HDFC customers find the onboarding frictionless. Complimentary travel insurance coverage varies by card variant — confirm with your branch exactly what’s covered before you depart.

Workable for HDFC customers who value the relationship and support infrastructure. Not competitive on fees versus the zero-markup alternatives. If fee minimisation is your primary goal, the cards above win on cost.

Thomas Cook Borderless Travel Card — Best for Full-Service Travel

Thomas Cook has been in the forex business longer than most fintech apps have existed. The Borderless Travel Card loads up to 12 currencies. Insurance coverage runs up to ₹7,50,000 on the One Currency card variant; the Study Buddy card (specifically designed for students going abroad) covers up to $10,000. ATM acceptance spans 1.9 million Mastercard ATMs and 31.4 million merchant establishments globally (Mastercard network data).

What Thomas Cook offers that fintechs don’t: physical outlets in 200+ Indian cities for same-day card issuance and face-to-face reloads. If you’re departing tomorrow and discovered you don’t have a forex card yet, Thomas Cook’s walk-in counter is your option. That immediacy has real value.

Fees aren’t the sharpest — you pay a service premium for the branch infrastructure and insurance depth. For senior travellers, first-time international travellers, or parents setting up a student abroad, that trade-off is fair. The Study Buddy variant specifically is worth investigating for students heading to the UK, US, or Australia.

Best for travellers who value physical support, insurance depth, and the option to walk into a branch. Thomas Cook Borderless isn’t the cheapest option, but it’s the most full-service in the traditional forex card segment.

SBI Multi-Currency Foreign Travel Card — Best for SBI Customers

SBI’s multi-currency travel card supports 7 currencies with zero annual maintenance fee — a genuine differentiator among public sector bank forex products. The Mastercard network delivers 34.5 million merchant acceptance points globally. Card validity runs 5–7 years.

Issuance fee: ₹100 + GST. Reload fees vary by amount and currency. Cross-currency conversion fees apply outside the 7 loaded currencies — that’s the limitation to know going in. No zero-markup offering in the standard variant.

If you bank with SBI and travel primarily to major western destinations (USA, UK, Europe, Australia), the 7-currency coverage is sufficient. The zero AMC and the wide merchant network make it a functional card for occasional travellers who don’t want to open accounts at a separate provider.

Solid baseline option for SBI customers. Not built for the cost-conscious frequent traveller, but low-friction for existing SBI account holders who travel once or twice a year.

What Is the Best Forex Credit Card in India with Zero Markup?

Forex prepaid cards and zero-markup credit cards are different products, but both solve the same problem: eliminating conversion fees on international spending. Several credit cards now offer true zero markup on foreign transactions.

- Federal Bank Scapia Credit Card — Zero forex markup, no annual fee, cashback on international transactions. One of the cleanest zero-markup credit options currently available to Indian cardholders.

- IDFC FIRST Mayura Credit Card — Zero markup, complimentary international lounge access, reward points on overseas spends. Annual fee waived on meeting a spend threshold.

- RBL Bank World Safari Credit Card — Zero forex markup on international transactions, 2 reward points per ₹100 spent abroad, complimentary lounge access at selected airports.

The honest reality: zero-markup credit cards suit travellers who pay their balances in full every month. If you carry a balance, the interest charge — typically 36–42% annualised — swamps every rupee saved on the markup. For disciplined spenders, these cards work well for large purchases, hotel deposits, and rental car holds where a prepaid card’s balance may be tied up for days.

From my own experience covering forex markets and travelling across Southeast Asia on a reporting assignment, I loaded a zero-markup card in Singapore dollars and Malaysian ringgit before departure. The saving versus using my regular ICICI debit card was approximately ₹4,200 over 12 days on a modest daily budget. Not abstract arithmetic — ₹4,200 is a night at a decent guesthouse in Penang. That’s what markup fees cost in practice.

Forex Card vs Credit Card vs Cash — What Should You Actually Carry?

Carry all three, weighted toward the forex card. That’s the practical answer.

- Forex card covers your daily spending — hotels, restaurants, retail, transportation. Zero markup on loaded currencies, predictable spend, no statement shock. Load it before you fly at a rate you’ve locked in.

- Credit card (zero markup if possible) handles large purchases, hotel pre-authorisations, and rental car holds. It’s also easier to dispute fraudulent charges on a credit card than on a prepaid card — the liability framework is different. Make sure it has zero forex markup, or you’re paying the conversion tax on every swipe.

- Cash — a modest amount for taxis, street food, small vendors, and any destination where card terminals are unreliable. Southeast Asia, Eastern Europe, and rural areas across multiple continents still run heavily on cash. Don’t arrive with zero cash on the assumption that your forex card will handle everything.

What you shouldn’t do: use your regular Indian debit card abroad without checking the forex markup. Most public sector bank debit cards charge approximately 3% conversion on every international transaction. That’s ₹3,000–₹3,500 in invisible fees on a ₹1 lakh trip.

Dynamic currency conversion (DCC) is a separate trap worth flagging. When a merchant terminal abroad offers to charge you in Indian rupees, decline. Their exchange rate is typically 5–7% worse than the card network rate. Always pay in the local currency, no exceptions.

What Do RBI Rules Say About Forex Cards in India?

TheReserve Bank of Indiasets the regulatory framework for all outward foreign exchange through the Liberalised Remittance Scheme (LRS). A few limits every forex card user should know:

- Annual limit: $250,000 per individual per financial year. This cap covers all outward forex — travel, education, investment, gifts, and maintenance combined.

- Cash limit: Transactions below ₹50,000 per transaction can be settled in cash. Above that, payment must go through a banking channel.

- Retention limit: After returning to India, you can retain up to $2,000 equivalent in foreign exchange. Amounts above that must be converted to rupees or redeposited within 180 days.

- Tax Collection at Source (TCS): Following Budget 2025, the TCS threshold on outward LRS remittances was raised from ₹7 lakh to ₹10 lakh per financial year, effective April 1, 2025; forex card loads are included in this calculation. No TCS applies on LRS transactions up to ₹10 lakh annually. Above ₹10 lakh, a 5% TCS applies on non-education remittances. Education and medical remittances are taxed at 2% above the threshold, and education remittances funded by loans from recognised financial institutions are exempt from TCS entirely. TCS isn’t a final tax, you can claim it back against your income tax liability via Form 26AS, but timing your loads across a financial year matters. If you’re loading large sums onto a forex card for a year studying abroad, speak to a CA about the implications before you start.

“Students have again started applying for universities abroad. They have to remit their fees and maintenance, living expenses — which contributed to a significant amount of rise. Plus, there are other reasons like remittances by small and medium enterprises.” — Ravindran Menon, CEO of RemitX (a division of Capital India Finance Ltd)

This TCS provision is the most frequently missed element in forex card planning. The ₹10 lakh threshold gives more headroom than the previous ₹7 lakh limit, but it still arrives faster than most people expect when you’re covering tuition instalments, accommodation, and living expenses across a full academic year.

How Do You Apply for a Forex Card in India?

The process is straightforward. Banks and forex providers have tightened digital onboarding considerably in 2024–2026.

For most cards, the five-step process looks like this:

- Step 1 — Choose your card based on the criteria above. Currencies needed, fee tolerance, whether you want a physical branch option.

- Step 2 — Gather documents: PAN card, valid passport, visa copy (if the destination requires one), confirmed air ticket, Aadhaar.

- Step 3 — Apply online or in-branch. Wise, Niyo, and BookMyForex are fully digital — apply, upload KYC documents, and receive the card by courier. HDFC, Thomas Cook, and SBI can be processed online or in-branch; Thomas Cook’s 200+ physical locations offer same-day issuance for urgent departures.

- Step 4 — Load the currency at the current exchange rate. For zero-markup cards, the rate you load at is the rate you spend at.

- Step 5 — Activate before travel. Most cards require activation through the app or a first transaction in India.

For Wise specifically, KYC is handled entirely through the app — upload your PAN, passport, and a selfie. Approval typically comes within one to three business days. Thomas Cook’s foreign exchange counter at Connaught Place in Delhi or Nariman Point in Mumbai will issue on the same day for same-day or next-day departures.

Conclusion

Choosing the best forex card in India comes down to matching the card to your travel pattern, not picking the loudest brand. For zero-markup global travel, Wise leads on transparency and app experience; Niyo Global wins on currency breadth (130+); BookMyForex is the purist’s option with no fees across four cost dimensions. HDFC, SBI, and Thomas Cook earn their place for relationship banking, public sector access, and walk-in support respectively. Whatever you choose, watch RBI’s LRS limits and the updated TCS threshold (₹10 lakh) before loading large sums. The right card pays for itself on a single international trip.

Frequently Asked Questions

1. Which forex card is best for travel in India in 2026?

For most travellers, Wise and BookMyForex offer the best combination of zero markup and practical currency coverage. Wise has the edge on app experience and global reach (40+ currencies). BookMyForex wins on pure fee elimination across all four cost dimensions.

2. Is there a best forex card in India with zero markup?

Wise, Niyo Global, and BookMyForex all offer zero markup on loaded currencies. In the credit card category, Federal Bank Scapia and IDFC FIRST Mayura offer zero markup on international purchases with no annual fee (Scapia) or a waivable annual fee (Mayura).

3. Can I use a forex card for online shopping abroad?

Yes. International e-commerce sites billing in a currency you’ve loaded work seamlessly. For Indian websites billing in INR, your regular debit or credit card makes more sense — forex cards aren’t designed for domestic rupee transactions.

4. What happens if I lose my forex card abroad?

Block it immediately through the card’s app — Wise and Niyo both support instant freeze via mobile. For HDFC and Thomas Cook, the international helpline number is printed on the back of the card and available on the provider’s website. Once blocked, request an emergency replacement or a virtual card number for immediate use.

5. How much can I load on a forex card in India?

Annual loading across all forex transactions is subject to the RBI LRS cap of $250,000 per financial year. Individual card loading limits vary — typically $10,000–$50,000 per transaction, with annual ceilings aligned to RBI. Remember the ₹10 lakh TCS threshold (raised from ₹7 lakh in Budget 2025) described in the RBI section above.

6. Are forex cards better than cash for international travel?

For most destinations, yes. Zero-markup forex cards give you near-interbank exchange rates, protection against theft, and ATM access where you need it. The exception is remote destinations with unreliable ATM infrastructure — carry cash as backup in those situations, and factor in any ATM withdrawal fees before you rely on machine access.

7. Which is the best forex card in India for students?

Thomas Cook’s Study Buddy card is built specifically for students abroad, with $10,000 insurance cover and multi-currency loading across major study destinations. Wise and Niyo Global are strong alternatives for students comfortable with app-based management who want zero markup on day-to-day spending.