You’re standing at an ATM in Barcelona on day two of your trip. The machine quotes €200. Fine. What doesn’t flash on the screen: your bank already marked up the exchange rate by 2.75% before you hit confirm, and there’s a £3.50 withdrawal fee stacked on top. That €200 just cost you roughly £14 more than the mid-market rate said it should.

This is the default for most travelers using a standard high-street debit card abroad. The costs are real and they’re spread across enough separate line items that they’re easy to miss until the statement arrives home. This stands valid only when you don’t know the differences in terms of use of Forex Card vs Debit Card.

I’ve watched a €200 withdrawal in Lisbon land on my statement nearly £15 above the rate my phone showed that morning — which is exactly why I now load a card before any trip longer than a week.

Forex cards, prepaid multi-currency cards loaded before you fly, were built to cut out most of this. Whether they actually do depends on which debit card you’re comparing them against, and how you travel.

How Your Debit Card Charges You Abroad

Your debit card abroad isn’t just reaching into your account. It’s running every transaction through a currency conversion system that takes a cut at multiple points.

- Layer one: the exchange rate markup. Most major banks convert at 2.5–3.5% above the mid-market rate — the interbank rate you’d see on Google or XE. That gap is pure bank margin, applied to every single foreign-currency transaction you make.

- Layer two: the cross-currency transaction fee. Some banks add 1–1.5% on top as a separate processing charge. It’s distinct from the rate markup — a second line item, not always displayed clearly. You may only spot it by downloading your full statement and doing the maths yourself.

“they charge a margin on the exchange rate, which is a hidden cost”

— Shrawan Saraogi, APAC head of expansion, Wise

- Layer three: the ATM fee. Major US and UK banks typically charge $3–5 (or the equivalent) per overseas ATM withdrawal, separate from any fee the local ATM operator charges. Four withdrawals over a two-week trip adds $15–20 in fees you’d rather not pay.

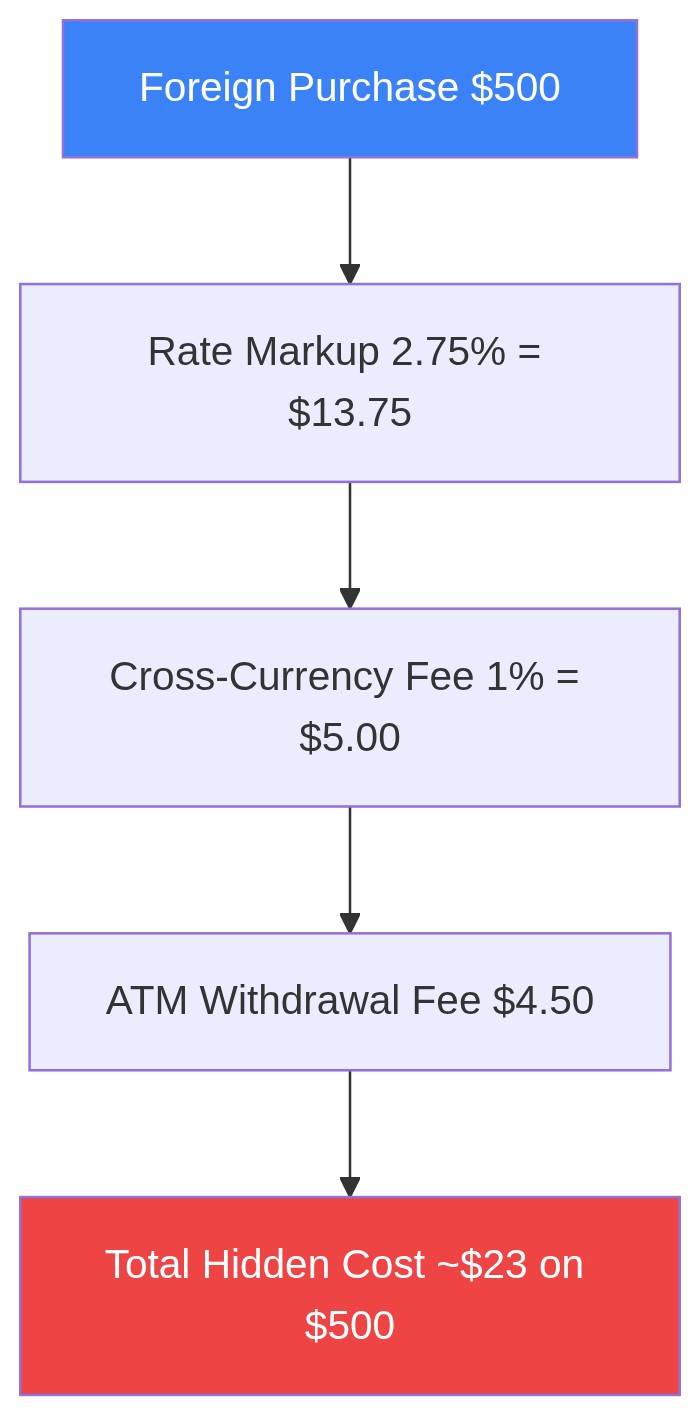

Run the numbers on $500 spent in a day: a 2.75% markup plus a 1% cross-currency fee plus a $4.50 ATM fee works out to around $24 in charges. On a $3,000 trip, that compounds into something worth taking seriously before you leave.

What a Forex Card Does Differently

A forex card is preloaded with the destination currency. Spend euros from a euro-loaded card, and there’s no conversion happening at checkout — the conversion occurred when you loaded the card. One rate. One event. Done.

Cross-currency fee: gone. No conversion at the point of purchase means no cross-currency charge.

Rate markup at loading: much smaller. Forex card providers typically charge 0.5–2% above mid-market at loading — against the 2.5–3.5% hit on every debit card swipe. That’s the core saving, and it compounds across every transaction on the trip.

ATM fees: lower, not zero. Most forex cards still charge per overseas withdrawal — often $2–2.50 per transaction. That’s cheaper than a typical bank’s debit card fee, but it’s not free. Worth factoring into the comparison.

The underrated feature: rate lock. Load your card today, and that’s the rate you spend at for the whole trip. If your home currency weakens mid-journey, the card rate doesn’t move with it. For longer trips or students living abroad, that certainty is genuinely useful.

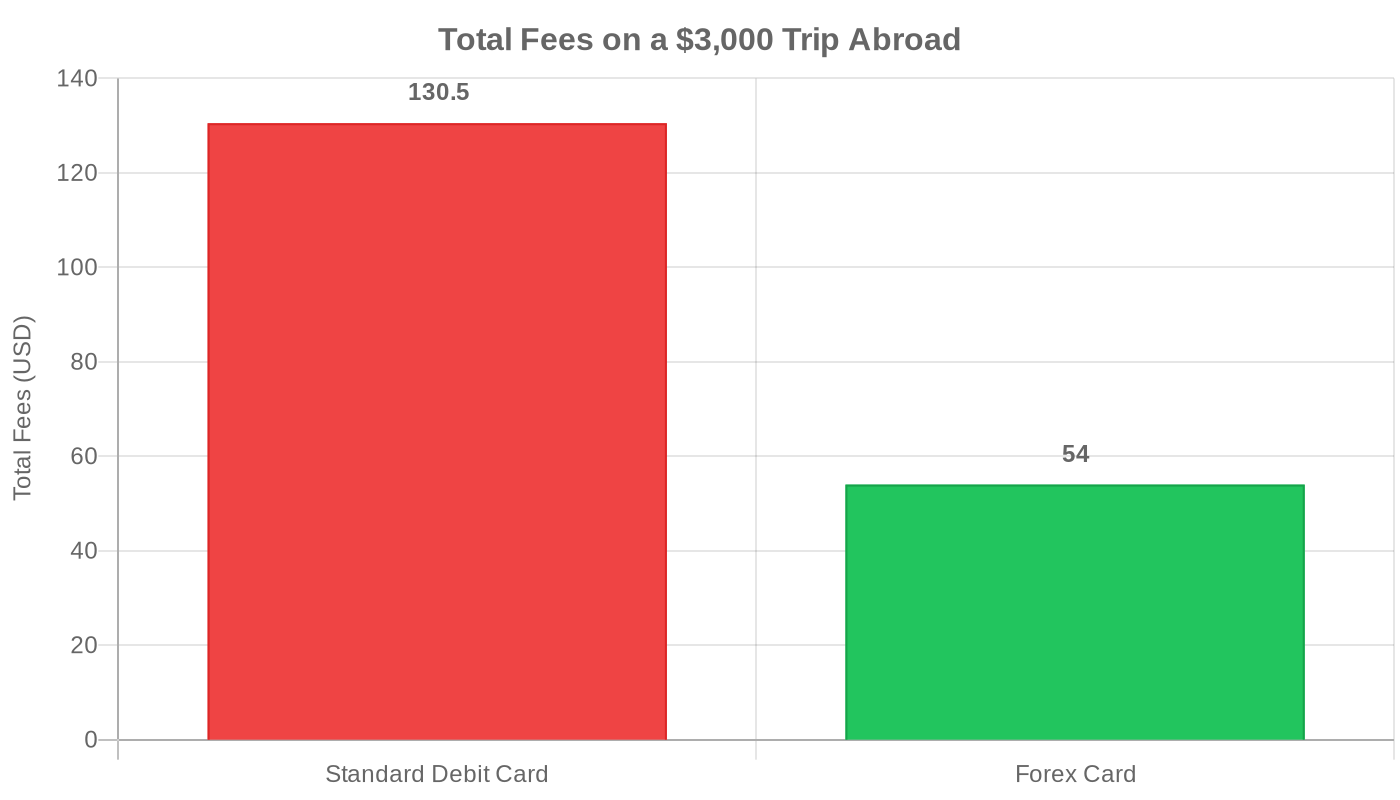

The Real Cost of Forex Card vs Debit Card — A $3,000 Trip Compared

Take a standard 10-day trip with $3,000 in local currency spending across dining, transport, shopping, and cash withdrawals. Here’s how the two card types compare:

| Fee Type | Standard Debit Card | Forex Card |

|---|---|---|

| Exchange rate markup | 2.75% = $82.50 | 1.5% at loading = $45.00 |

| Cross-currency fee | 1% = $30.00 | None = $0.00 |

| ATM fees (4 withdrawals) | 4 × $4.50 = $18.00 | 4 × $2.25 = $9.00 |

| Total fees | $130.50 | $54.00 |

| Net saving vs debit card | — | $76.50 |

The $76.50 saving is a mid-range estimate. Banks with 3.5% markups push the debit card total above $175. Banks on the opposite end — Wise, Starling, and Charles Schwab International — bring debit card costs down to near-forex-card levels. The honest question to answer before you travel: which category does your current debit card fall into?

Check your bank’s foreign transaction terms. If they’re not listed prominently in the app, that’s usually a sign the number isn’t flattering.

When Your Debit Card Makes More Sense

Short trips narrow the gap fast. If you’re spending $500 over a long weekend, the $76 saving scales down to around $12 — and the admin friction of loading a forex card, managing leftover currency, and carrying an extra card may not be worth it.

Modern low-fee debit cards close the gap entirely. Wise, Starling, and Monzo in the UK; Schwab International in the US — these accounts offer mid-market or near-market rates with minimal ATM fees. If you’re already on one of them, you’re getting forex card rates without a second card.

Flexibility is the debit card’s real advantage. No pre-loading decisions. No mental maths about how much local currency you’ll need for two weeks in three different countries. Direct access to your account balance, whenever you need it. For spontaneous travel or destinations where spend is hard to predict, the debit card is simpler.

One risk that applies to both cards: dynamic currency conversion, or DCC. Foreign ATMs and merchants sometimes offer to charge you “in your home currency for your convenience.” Always decline. The rate they use is typically 3–7% above mid-market — enough to wipe out the forex card advantage entirely if you keep saying yes.

“decline the currency conversion offer and report the incident to your card issuer”

— Visa UK, official DCC guidance

Which Card Should You Take?

For trips of a week or more on a standard bank account, the forex card wins on cost. It’s not marginal. On a $3,000 trip, $76 covers a train connection, a museum visit, or two decent restaurants. That’s money that otherwise goes to your bank for doing very little.

The setup takes 15 minutes: load a multi-currency forex card in your destination’s primary currency before you fly. Keep the debit card in your wallet for genuine emergencies — lost card, unexpected account access need. That’s it.

If you’re already on Wise, Starling, or Schwab, you don’t need the forex card. Those accounts already deliver competitive rates.

On a recent three-country trip I carried both: the forex card handled everything predictable, and the debit card sat untouched until a hotel pre-auth needed it.

If you’re on a high-street bank with standard fees and you haven’t checked the foreign transaction terms in the last 12 months: check them. Then decide whether a $76 saving over a 10-day trip is worth the pre-trip effort. Most people who do the maths switch.

Conclusion

The forex card vs debit card decision really comes down to two things: how long you’re travelling, and which debit card you already hold. For trips of a week or more on a standard high-street account, a forex card’s lower loading markup and cheaper ATM withdrawals save real money — enough to notice on a $3,000 trip. But if you already carry a low-fee account like Wise, Starling, Monzo or Schwab, you’re effectively on forex-card rates already, and a second card just adds admin. Either way: check your current terms, decline dynamic currency conversion every time, and always pay in the local currency.

FAQ: Forex Card vs Debit Card Abroad

1. Is a forex card cheaper than a debit card abroad?

For most travelers on standard bank accounts, yes. Forex cards charge 0.5–2% at loading; debit cards charge 2.5–3.5% per transaction. On a $3,000 trip, that gap runs to $50–$120 before ATM fees are counted. If you hold a zero-markup debit card such as Wise or Starling, the saving narrows to the point where it may not justify the extra admin.

2. Do forex cards have ATM fees overseas?

Most do — typically $2–2.50 per withdrawal. Some providers include a set number of free overseas withdrawals per month; check the specific card terms before you rely on it. That said, $2.25 versus $4.50 still represents a saving on every cash withdrawal you make.

3. What happens to leftover money on a forex card after the trip?

Most providers let you convert unused foreign currency back to your home currency or transfer to a linked account, usually at a small fee. Some charge dedicated encashment fees. Read the exit terms before loading — leftover currency at an unfavorable conversion can chip away at the savings you made during the trip. Load conservatively if you’re unsure about spend.

4. Should I use my forex card or debit card for a large hotel bill?

Forex card. Large transactions amplify every percentage point of markup difference. A $1,000 hotel bill at 3.5% costs $35 more than at 0.5%. That’s real money worth routing through the better-rate card. One caveat: some hotels hold a pre-authorisation deposit on the card — check in advance whether your forex card handles holds without freezing the full pre-auth amount rather than just reserving it.

5. Can I use a forex card at any ATM abroad?

Any ATM accepting Visa or Mastercard, depending on the network your forex card runs on — which covers the vast majority of cash machines globally. Local ATM operators may still apply their own fee on top of your card’s withdrawal charge. That’s the operator’s decision, not your card provider’s, and it applies equally to debit and forex cards.