Forex Card vs Cash for International Travel: The Honest Breakdown

Picture this: you land in Bangkok at 10 PM, phone at 3%, and the airport exchange counter is the only game in town. The rate on the board is 10% above interbank. You know you’re being fleeced. You hand over the cash anyway because there’s no alternative standing between you and a taxi into the city.

That’s the trip opener most travellers experience exactly once. After that, they plan better.

The core question: forex card vs cash, which one should be chosen, sounds simple. The answer isn’t. Costs, risks, and practical realities differ enough between the two that the wrong call on a two-week holiday can cost you several hundred dollars you didn’t need to spend.

Forex Card vs Cash: Quick Reference

| Factor | Forex Card | Cash |

|---|---|---|

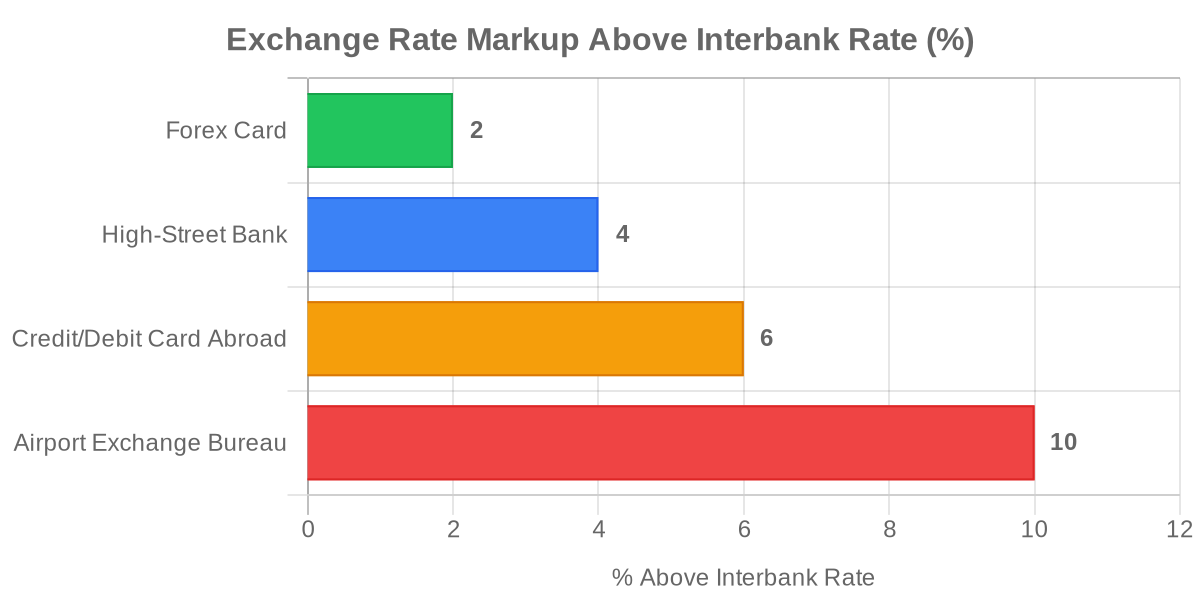

| Exchange rate | 1–3% above interbank | 3–12% above interbank |

| Security if lost | Blockable, replaceable | Gone permanently |

| Acceptance | Terminals and ATMs (Visa/Mastercard) | Universal |

| ATM fees | $2–$5 per withdrawal | Depends on source provider |

| Best for | Hotels, restaurants, larger purchases | Markets, tips, rural areas |

| Card terminal required | Yes | No |

| Currency risk | Locked at loading | Rate varies at point of exchange |

What Is a Forex Card and How Does It Work?

A forex card is a prepaid travel card loaded with foreign currency before you leave home. You can read a full breakdown of how they work in PipPenguin’s forex card guide, but the short version: it functions like a debit card at your destination, you swipe it at merchants, tap at contactless terminals, or use it at ATMs. The exchange rate is locked at the time of loading, which means you’re not exposed to whatever the currency does while you’re sitting on a beach.

Most multi-currency cards support 10–15 currencies on a single card. Load euros for Paris, dirhams for Dubai, baht for Bangkok, all on one piece of plastic. You can top up remotely if you run low. The loading rate, not the daily spot rate, is what you get charged.

That’s the basic mechanics. The more interesting question that I want to ask is what it actually costs you versus carrying foreign notes.

Exchange Rates: Where Forex Cards Win

This is where most travellers leave money on the table. Genuinely, quietly, every trip.

Airport currency exchange bureaus routinely price 7–12% above the real interbank rate. On a $3,000 travel budget, a 10% markup costs you $300 before you’ve checked in to your first hotel. That isn’t a rounding error, that’s a decent one-night stay or two flights’ worth of luggage fees, gone.

Forex cards loaded through reputable providers typically run 1–3% above interbank. That’s the margin covering their costs, not extracting maximum profit from time-pressured travellers.

Forex cards loaded at a competitive provider typically carry a 1–2% spread above the interbank rate, compared to 7–12% at airport exchange bureaus. On a $3,000 travel budget, that gap translates to $150–$270 per trip. The rate on a forex card is also locked at loading, protecting the cardholder from in-trip currency movements. (Industry estimates, Q1 2026)

Cash from a reputable bank or online FX provider booked a week in advance can sometimes match card rates. The problem is most people don’t book ahead. They exchange at the airport because it’s there and the queue looks short. That convenience is what costs $200–$300 on a typical holiday.

Security: Not Even Close

Cash that walks out of your wallet doesn’t come back. There’s no dispute process, no fraud team, no refund. Someone lifts your wallet in a Barcelona market and whatever you were carrying is simply gone.

Forex cards flip this entirely. Block it through the app or provider helpline. Request a replacement. The remaining balance transfers to the new card. You’re down the inconvenience, not the money.

ATM fraud exposure is also contained in a way your main bank account isn’t. You’re drawing from a loaded balance. A compromised card drains only what you put on it, not your savings.

One caveat worth stating plainly: the card-blocking process takes time. You need a plan for the hours between losing the card and getting a replacement, which is exactly why carrying a small cash reserve of $50–100 makes sense even when you’re primarily using a card.

Where Cash Still Wins

I will tell you, cards don’t always work. That’s the part no one mentions in the glossy comparison articles.

Street food stalls in Ho Chi Minh City. Tuk-tuks in Chiang Mai. Market vendors in Marrakech. Many of these operate cash-only, not because they’re behind the times, but because card terminals cost money to run and the economics don’t stack up for a $1.50 noodle bowl.

Rural areas in developing markets regularly have unreliable infrastructure. Power cuts, network dropouts, old terminals that won’t read chip-and-PIN. You don’t want to discover this at a guesthouse check-in at midnight.

Then there’s tipping. In cash-tip cultures, the US, Mexico, most of Southeast Asia, handing someone a card reader for a $2 tip is awkward at best and impossible at worst. Waitstaff, bellhops, tour guides, housekeeping: cash is still how you say thank you.

The takeaway isn’t “carry as much cash as possible.” The conclusion is much simpler: don’t travel with zero.

ATM Fees: The Hidden Cost of Forex Cards Abroad

This is where the forex card’s advantage quietly erodes if you’re not careful.

Every ATM withdrawal on a forex card typically costs $2–$5 in flat fees. Per transaction. Pull out cash five separate times and you’ve paid $10–$25 in fees before the exchange rate even enters the picture.

Cross-currency conversion adds another layer. If your card is loaded in euros but you tap for a Swiss franc payment, the cross-conversion charge hits — typically 4–4.5% on most multi-currency cards. Load the card in your destination’s currency and this doesn’t apply. On a multi-country trip it’s an easy mistake, so it’s worth loading each currency separately before departure.

The practical move: withdraw once, in a larger amount, at an ATM inside a bank branch rather than at an airport kiosk. One $500 withdrawal at a $3 fee beats five $100 withdrawals costing $15 total. The math is obvious once you see it.

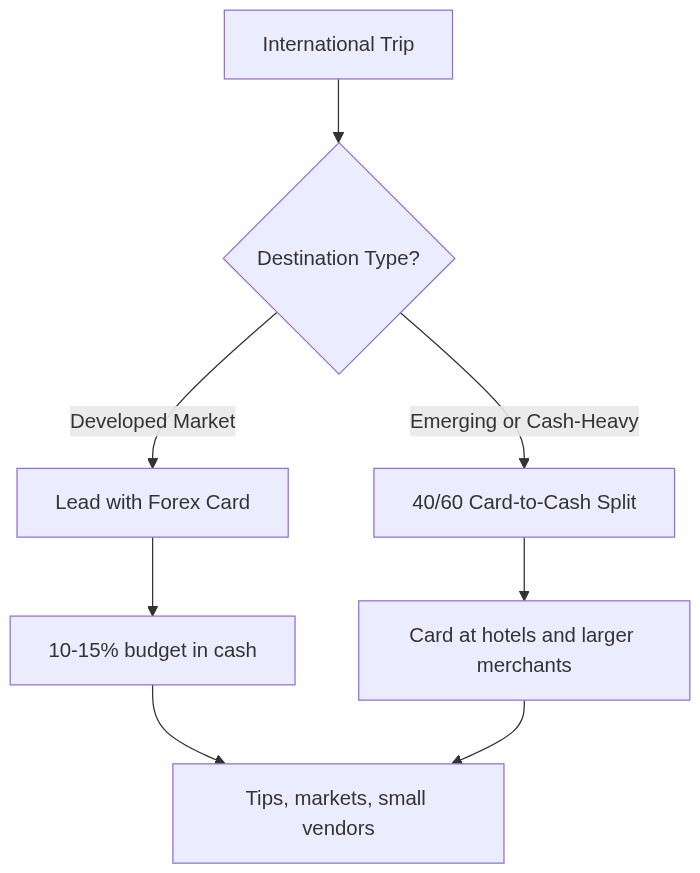

Decision Framework: Which Destination, Which Approach?

There’s no single answer that works for every trip.

- Developed markets — Western Europe, the US, Australia, Japan, card infrastructure is excellent and contactless is near-universal. Lead with your forex card. Keep €100–200 equivalent in cash for tips, street markets, and small vendors. That’s roughly 10–15% of a typical week’s holiday budget.

- Emerging and cash-heavy markets — Southeast Asia, parts of Latin America, Africa, rural Eastern Europe, cash still dominates large portions of daily commerce. A 40:60 card-to-cash ratio is more realistic. Use the card at hotels, larger restaurants, and city-centre shops; cash covers everything smaller than a sit-down meal.

- Airport arrivals, everywhere — exchange bureaus at airports are the worst-rate option on the planet, consistently. Either carry your foreign currency loaded on the card before you fly, or withdraw from an ATM once you’re through arrivals. Never exchange at the airport bureau if you can avoid it. For Indian travellers specifically, PipPenguin’s guide to RBI-approved forex apps covers compliant ways to load travel cards before departure.

Conclusion

Forex card for the bulk of your spend. Cash for the edges — tips, markets, places where terminals don’t exist. That’s the sensible position and it isn’t particularly close.

What catches people out is the airport exchange decision. The rate gap between loading a forex card a week before departure versus exchanging at the arrivals hall typically runs 7–9 percentage points. On a $3,000 holiday budget, that’s $210–$270 you handed over for no good reason. Most travellers make that call once, feel the sting, and never repeat it.

Load the card mid-week before departure — bank desks are most active Tuesday through Thursday and rates tend to be tighter than on Fridays or weekends. If you’re heading somewhere cash-heavy, source local currency from your home bank or an online provider at the same time. Carry 15–20% of your daily budget in cash for small transactions and tipping.

Check your card provider’s ATM fee schedule before you go. Not all forex card providers charge the same rates, some waive withdrawal fees for premium-tier cards, and knowing this before you’re standing at an ATM in Bangkok is considerably more useful than finding out afterwards.

The forex card wins on cost and security for most of what you’ll spend. Cash wins on universality. The traveller who uses both, deliberately, in the right ratio for their destination, comes out ahead on both counts.

Frequently Asked Questions

1. Is a forex card better than cash for international travel?

For most destinations with solid card infrastructure, yes. Forex cards lock your exchange rate at loading and typically cost 1–3% above interbank — compared to 7–12% at airport exchange bureaus. Security is also stronger: a lost card is blockable, whereas lost cash is simply gone. For rural destinations or cash-heavy economies, carrying additional physical currency is still essential, so a hybrid approach gives you the best of both.

2. How much cash should I carry alongside a forex card?

In developed markets — US, Europe, Australia — 10–20% of your trip budget in cash is enough to cover tips, markets, and small vendors. In Southeast Asia, parts of Africa, or other cash-heavy economies, 30–40% is more realistic. Anything beyond that and you’re taking on unnecessary security risk carrying currency you don’t need.

3. Can I use a forex card at any ATM abroad?

Most forex cards run on Visa or Mastercard networks, meaning any ATM displaying those logos will accept them. Fees still apply — typically $2–$5 per withdrawal. Minimise your total fee spend by withdrawing in larger amounts less frequently rather than topping up in small amounts often.

4. What happens if I lose my forex card abroad?

Block it immediately through the app or the provider’s 24-hour helpline. Most providers can issue a replacement within 2–5 business days or transfer the remaining balance to a backup card if you registered one. This is exactly why carrying a small cash reserve of $50–100 matters even when you’re primarily card-based — it covers the gap.

5. Do forex cards charge fees when spending in a different currency?

Yes. If the card is loaded in euros and you spend in Swiss francs, a cross-conversion fee applies — typically 4–4.5% on most multi-currency cards. The fix is straightforward: load each currency you need before departure. On a single-country trip this is a non-issue; on a multi-country itinerary it’s worth planning in advance.