Forex Card Charges: Hidden Fees You Should Know

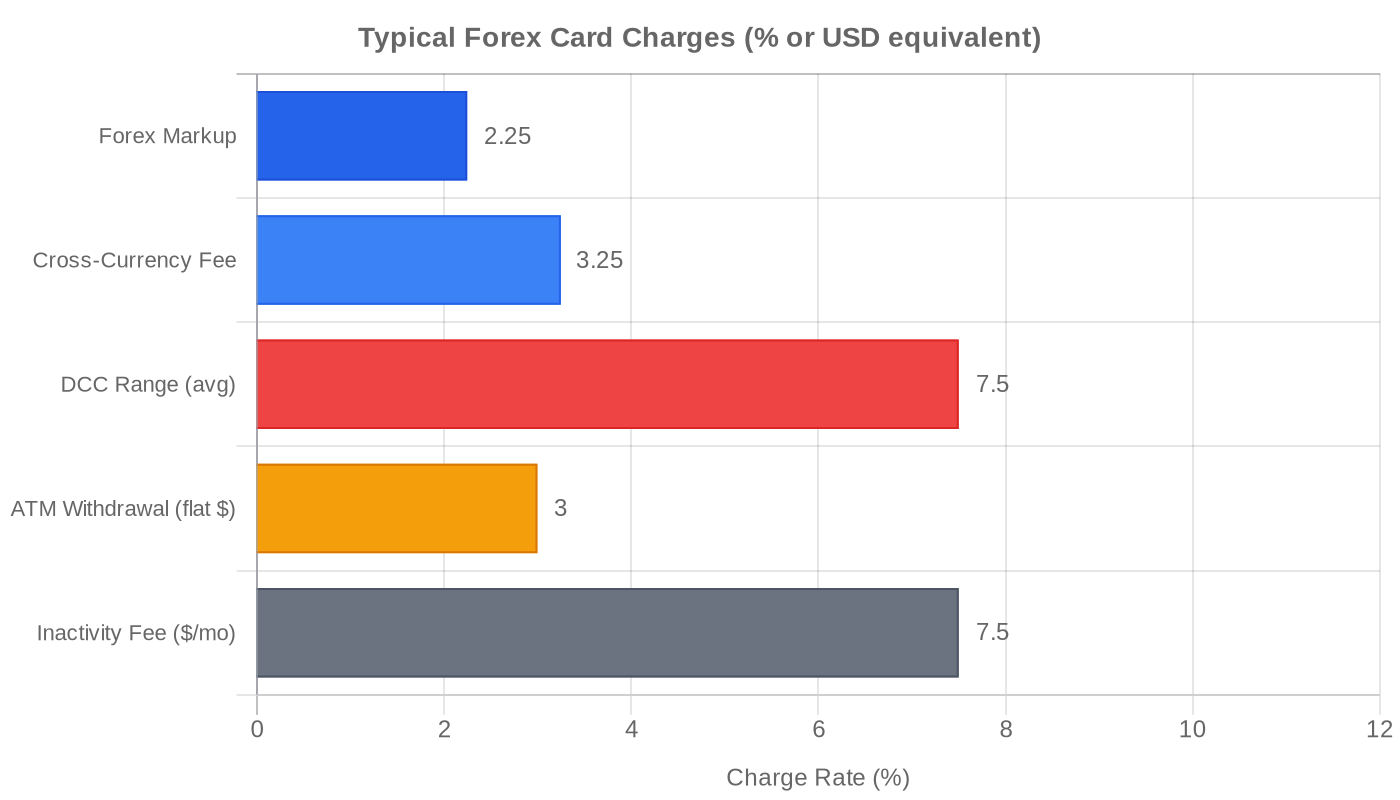

Forex cards carry at least five charge types most travelers never see at signup: a markup fee (1–3.5%) embedded in the exchange rate, cross-currency fees (~3%), ATM withdrawal fees ($2–$4 flat per use), balance inquiry fees (~$0.50), and inactivity charges after 180 days of non-use. The biggest hit is Dynamic Currency Conversion — a merchant-side conversion that can run 3–12% above your card’s own rate. Picking the local currency at every terminal eliminates it entirely. (Grand View Research, 2024; Wise, 2026)

You’re at a checkout in Bangkok. The screen flashes up: Thai baht, or British pounds. You pick pounds — it feels cleaner, like you know exactly what you’re spending. What just happened is that you gave the merchant’s bank permission to convert that transaction at their rate, not your card’s rate. That’s Dynamic Currency Conversion, and it quietly added somewhere between 3% and 12% to your bill. Nobody mentioned it when they handed you the card.

That one moment illustrates how most forex card charges actually work. The fees aren’t fraudulent. They’re in the documentation. They’re just not in the summary.

What Are Forex Card Charges?

Forex cards split their costs into two buckets: the ones you can see and the ones you can’t.

Visible fees are disclosed upfront — issuance charges (₹300–₹1,000, roughly $4–$13), reload fees (₹75–₹100 per top-up), ATM withdrawal fees, and balance inquiry charges. They’re annoying, but at least they’re declared.

The invisible charges do more damage. The forex markup — typically 1% to 3.5% above the interbank rate — gets baked directly into the exchange rate your card receives. There’s no separate line on your statement. You just get a worse rate and have to reverse-engineer what you paid.

The global prepaid forex card market sat at USD 115.85 billion in 2023 and is growing at a 12.46% CAGR through 2031 (Grand View Research, 2024). More travelers are reaching for these cards. Fewer of them read the fee schedule before loading the first currency.

How Is the Forex Markup Fee Calculated?

The interbank rate is the rate banks trade at with each other. Nobody retail gets that rate. But it’s the benchmark — everything is priced off it.

Your card issuer takes the interbank rate and layers their margin on top. A 2% markup on a $1,000 spend costs $20. On a $5,000 trip, that’s $100 gone before a single ATM fee touches your balance.

The markup isn’t always called a markup. It shows up as a “currency conversion fee,” a “foreign transaction fee,” or — the most misleading version — folded into the “card rate” with no percentage shown anywhere.

Where the major issuers sit, as of early 2026:

| Card Type | Typical Markup |

|---|---|

| Traditional bank forex card | 2–3.5% |

| Co-branded fintech card | 1–2% |

| Zero-markup card (e.g., Niyo Global) | 0% markup (other fees still apply) |

| ICICI Bank cross-currency rate | 3.5% |

| Axis Bank cross-currency rate | 3.5% |

(Wise, 2026)

Frankly, I’ve checked enough forex card statements to say this with some confidence: the markup is the single biggest consistent cost most travelers never calculate. ATM fees sting once. The markup comes off every single transaction.

As Shrawan Saraogi, APAC head of expansion at Wise, points out, providers “charge a margin on the exchange rate, which is a hidden cost” (Business Standard, 2024) — the exact reason the markup never shows up as its own line.

The rate also compounds when you reload. Every top-up gets priced at the issuer’s spread on that day — which can be higher or lower than when you first loaded.

ATM Withdrawals Abroad: What Banks Actually Charge

Cash is still necessary in places where cards don’t work — local markets in Southeast Asia, smaller towns across Eastern Europe, rural East Africa. Using a forex card at an ATM is fine. The cost is just higher than people expect.

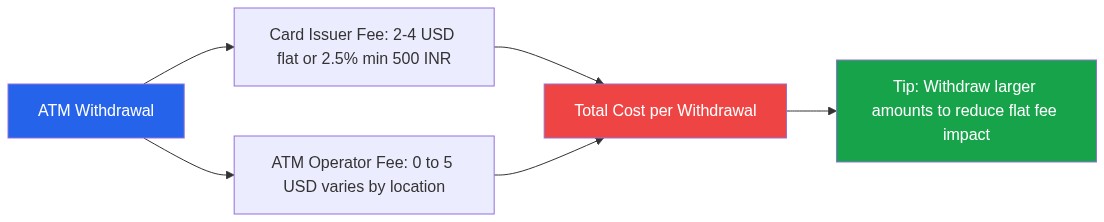

Most issuers charge a flat fee of $2–$4 per withdrawal. Some charge a percentage instead — typically 2.5% with a minimum of around ₹500 (roughly $6). Balance inquiries run about $0.50 per check.

That’s your issuer’s charge. The ATM operator also charges a local fee on top, which varies considerably — minimal at a major bank branch, as high as $5+ at standalone machines in airports or tourist zones. These two charges stack.

Two rules worth following: use ATMs at major bank branches rather than standalone machines in high-foot-traffic areas, and withdraw in larger amounts less often. Paying $2 on a $200 withdrawal is 1%. Paying $2 on a $40 withdrawal is 5%. The math isn’t complicated.

Cross-Currency Fees: When the Wrong Wallet Costs You

Multi-currency cards let you hold dollars, euros, and pounds in separate wallets on the same card. Useful for long trips across multiple countries. The catch: spending in a currency you haven’t loaded triggers a cross-currency conversion charge.

Say you loaded USD and your card gets charged in euros at a Paris restaurant. Your issuer converts the euro charge back to USD at their rate, then applies a cross-currency fee — typically 3–3.5% of the transaction. ICICI and Axis both charge 3.5% on this (Wise, 2026).

That applies every time you spend in an unloaded currency. A two-week trip through multiple European countries, using only loaded USD, can easily add up to ₹2,000–₹4,000 in cross-currency charges. Nobody’s doing that math in the moment.

The fix is straightforward: before you travel, load the currencies you’ll actually spend. On a multi-currency card, that’s just a matter of adding the right wallet before departure. You’re not buying separate cards — you’re adding wallets on the one you have.

Dynamic Currency Conversion: Say No Every Time

DCC is the most expensive mistake forex card users make consistently. It works because it looks helpful.

At a point-of-sale terminal abroad, the screen asks: pay in your home currency or local currency? Choosing your home currency gives you certainty — you can see the amount in familiar terms. The problem is that conversion is handled by the merchant’s acquiring bank at their rate. That rate runs 3–12% worse than your card’s own rate, depending on the merchant and location (Fi Money, 2026).

Always choose local currency. Every time. No exceptions.

I’ve held the DCC quote up against my card’s own rate on enough receipts to stop second-guessing it — the home-currency option has never once come out cheaper for me. The card networks agree: Visa’s own guidance tells travelers to “decline the currency conversion offer and report the incident to your card issuer” (Visa).

ATMs make the same offer. The machine will ask. It always asks. Decline the conversion and let your card handle it — even with a markup, your issuer’s rate is almost always better than what the ATM operator charges.

The Charges Nobody Mentions at Signup

Beyond markup, cross-currency, and ATM fees, a few more sit in the fine print:

- Inactivity fees. If your card goes 180 days without a transaction, most issuers start deducting a monthly charge. SBI charges 1.5 USD/month (Wise, 2026). Typical industry range: $5–$10 per month. Set a reminder when you get home — either spend residual funds, encash the balance, or make one small transaction before the 180-day clock runs out.

- Reload fees. Each top-up costs ₹75–₹100. That’s not much on one reload. On four or five small top-ups in a single month, it adds up to ₹300–₹500 in fees for the privilege of adding your own money to your own card.

- Card replacement. Lost or damaged cards typically cost ₹200–₹500 to replace. Some issuers charge considerably more — One Card, for instance, charges ₹3,000 for cancellation-related replacements (Wise, 2026).

These aren’t hidden in a deliberately deceptive sense. They’re in the schedule of charges. They’re just not on the marketing brochure.

How to Cut Your Forex Card Costs

You don’t need to switch cards to reduce what you pay. A few consistent habits make a real difference:

- Pay in local currency every time. This single decision eliminates DCC risk entirely.

- Load the right currencies before you go. Spending on a loaded currency avoids cross-currency fees. For a Europe trip, load euros before departure. Don’t top up in USD and let the card convert every transaction.

- Withdraw larger amounts less frequently. Flat ATM fees hurt most on small withdrawals. One $200 withdrawal costs $2. Five $40 withdrawals cost $10.

- Read your card’s actual fee schedule. HDFC’s Regalia ForexPlus and BookMyForex list every charge in full — this is the version to read, not the product landing page. If your issuer’s schedule is hard to find, that’s worth noting.

If your current card consistently charges above 2% markup, PipPenguin’s guide to zero forex markup credit cards covers the comparison clearly — including which zero-markup options still carry ATM and inactivity charges worth watching.

Robert’s Verdict: Forex Card Charges Aren’t a Mystery — They’re a Choice

Forex card charges are predictable once you know where the fee layers sit. The markup hides inside the exchange rate. DCC is an opt-in trap. Cross-currency fees fire every time the wrong wallet gets charged. And the inactivity clock starts the moment you land back home.

The cards themselves are still useful — they beat airport exchange bureaux on rate, and loading in advance protects you from mid-trip currency swings. The real job is knowing what the card costs before you commit to it, then doing three plain things: read the schedule of charges, load only the currencies you’ll actually spend, and pick local currency at every terminal.

For a full breakdown of how forex cards compare to travel credit cards and fintech alternatives, PipPenguin’s forex card guide covers the mechanics. Holding unused funds on a card after a trip? PipPenguin’s forex card to bank account transfer guide covers both online and offline options.

Frequently Asked Questions

1. What is a forex markup fee?

The forex markup is a percentage your card issuer adds on top of the mid-market exchange rate. It’s embedded in the rate you receive — not listed separately on your statement. Standard markups range from 1% to 3.5%. At 3% on a $1,000 transaction, that’s $30 in charges you won’t see itemised. Zero-markup cards eliminate this but often carry other fees in its place.

2. How much does a forex card ATM withdrawal cost?

Most issuers charge $2–$4 flat per withdrawal, or a percentage fee around 2.5% with a minimum floor (often ₹500). The ATM operator can add their own separate fee on top — this varies by country and machine type. Balance inquiries typically cost around $0.50. Withdraw larger amounts to reduce the per-transaction impact of flat fees.

3. What is a cross-currency fee on a forex card?

A cross-currency fee applies when you spend in a currency that isn’t loaded on your card. The issuer converts the charge at their rate and adds a fee — typically 3–3.5% of the transaction amount. ICICI and Axis Bank both charge 3.5% on these conversions. Loading the correct currency for each country before you travel is the cleanest way to avoid it entirely.

4. What is DCC on a forex card?

Dynamic Currency Conversion (DCC) occurs when a merchant or ATM converts your transaction into your home currency rather than local currency, using the merchant bank’s rate instead of your card’s rate. DCC rates typically run 3–12% above the interbank rate. Always select the local currency option at payment terminals — it avoids DCC and routes the conversion through your card issuer instead.

5. When do inactivity fees apply on a forex card?

Most issuers begin charging inactivity fees after 180 days without a transaction — typically $5–$10 per month. SBI charges 1.5 USD/month after hitting the threshold. Once you’re back from travel, either spend residual funds, encash the balance, or make one small transaction within six months to reset the timer. Holding a loaded, untouched card is a slow drain.