10 Forex Market Manipulation Examples That Made Headlines

The forex market trades over $7.5 trillion daily (Bank for International Settlements, 2022). That scale leads most traders to assume the market is too large to manipulate. It isn’t.

Some of the most brazen cases of market manipulation in financial history have targeted forex specifically. Not despite its depth, but because of it. Benchmark rates that ripple through trillions of dollars of global contracts. Central bank interventions that erase account balances in minutes. Traders using private client information to guarantee their own profits before a transaction even clears.

Each of the ten examples below was documented, prosecuted, and made global headlines. Some resulted in record-breaking fines. Others sent traders to prison. A few changed regulatory frameworks permanently. Understanding exactly what happened and how remains the most practical education any forex trader can get. In years of reviewing broker conduct and execution data, the cases that surprised me least were the ones insiders insisted were ‘just how the desk worked.’ That phrase is almost always the warning sign.

I believe there’s no shortage of theoretical manipulation scenarios, the real utility for traders is understanding exactly what has actually happened, how it worked, and what changed as a result.

What Is Market Manipulation?

Market manipulation is the intentional distortion of an asset’s price or volume through deceptive means, designed to benefit the manipulator at the expense of other participants.

“Fraudulent brokers may employ ‘price shading,’ deliberately skewing quotes by a few pips against the client during volatile periods, a practice nearly impossible for the retail trader to detect…” — Financial Industry Analysis (Ecole Intuit Lab)

The tactics vary. Placing large orders with no intention of executing them. Sharing confidential client order flow to coordinate positions across competing banks. Spreading false information to move prices before taking a position. What doesn’t change is the core move: manufacturing an artificial price signal, then trading against it for guaranteed profit.

Is Market Manipulation Illegal?

Yes, in every regulated financial jurisdiction. In the US, Section 9(a)(2) of the Securities Exchange Act of 1934 prohibits it. The EU’s Market Abuse Regulation (Article 12) covers it explicitly. In the UK, the Financial Services and Markets Act 2000 sets both civil and criminal thresholds.

The penalties are real. As the examples below show, fines can reach into the billions. Criminal convictions and prison sentences are not hypothetical outcomes reserved for edge cases, they happened, to traders at major banks, for conduct that many participants believed was standard industry practice.

“I didn’t know it was illegal” turned out to be a thin defense.

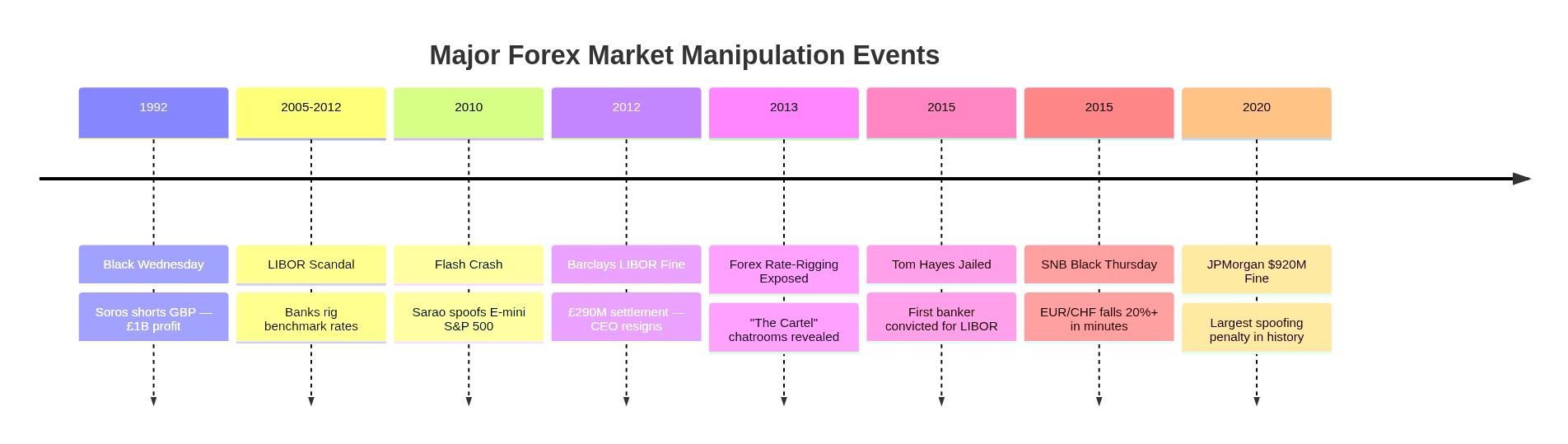

1. “The Cartel” — The Global Bank FX Rate-Fixing Scandal (2013–2015)

Start with the largest forex manipulation case in history.

From at least 2007 through 2013, traders at the world’s biggest banks colluded to rig the WM/Reuters benchmark exchange rates, the rates used globally to value portfolios, settle contracts, and benchmark pension funds. They did it via private chatrooms with names that tell you everything about the attitude involved: “The Cartel,” “The Bandits’ Club,” “One Team, One Dream,” “The Mafia.”

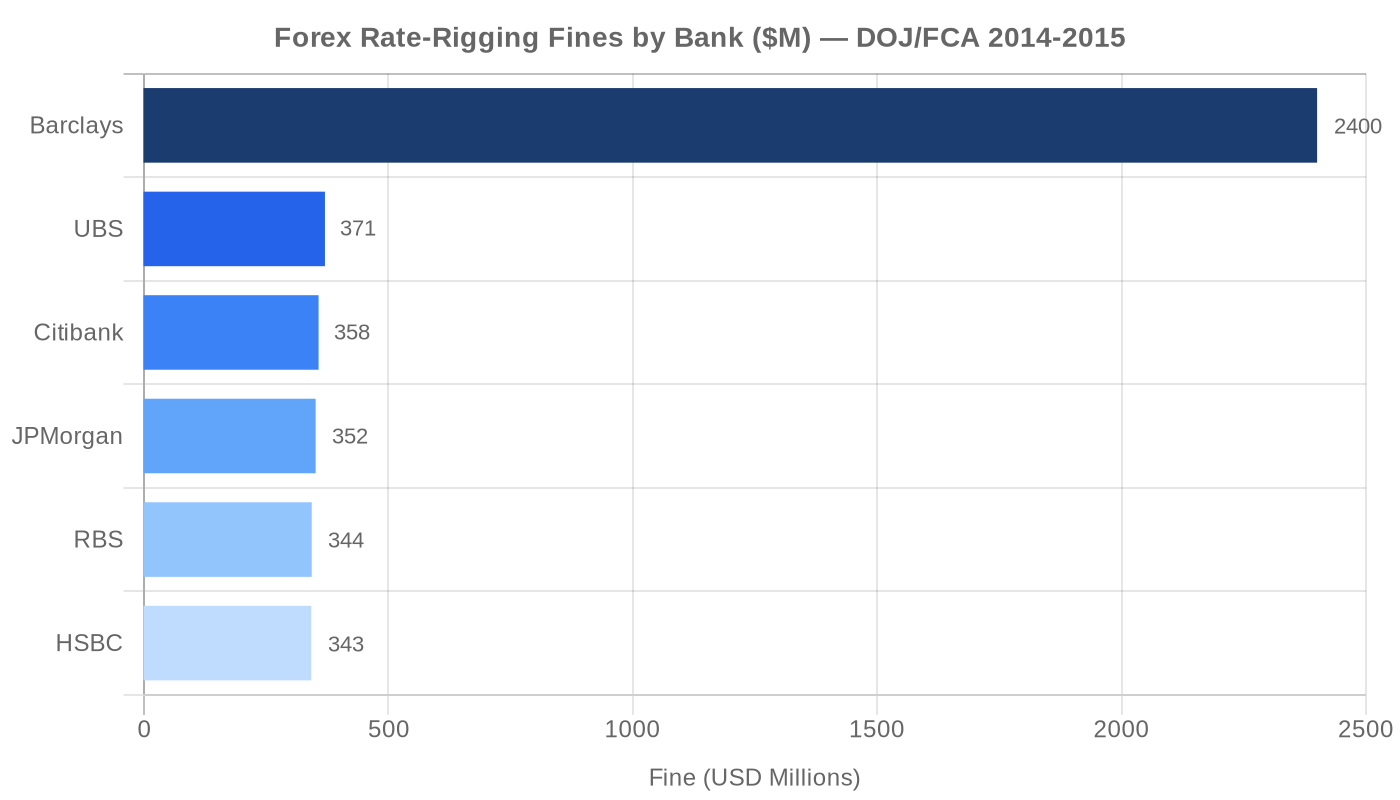

The mechanics were straightforward. WM/Reuters published its benchmark rates at 4:00 PM London time each day, calculated from a 60-second window of actual trades. Traders at Barclays, Citibank, JPMorgan, HSBC, RBS, and UBS shared client order flow ahead of this window. Confidential information they had no right to share. They coordinated to move rates in the direction that benefited their own positions. The estimated impact: approximately 30 pips per manipulation event, according to academic analysis of the period.

Britain’s 20.7 million pension holders were estimated to have lost $11.5 billion per year as a result(UK Financial Conduct Authority, December 2014)

The regulatory response, when it came, was significant. In November 2014, the FCA imposed $1.7 billion in fines across five banks. The CFTC levied $1.4 billion simultaneously. In May 2015, all six banks pleaded guilty to felony charges at the US Department of Justice, with Barclays separately fined $2.4 billion. Total penalties across all jurisdictions exceeded $10 billion.

Named individuals included Richard Usher (RBS senior trader, later JPMorgan), Rohan Ramchandani (Citigroup’s European spot trading head), and Chris Ashton (Barclays voice spot trading). Several traders were fired, though criminal convictions for individuals, as distinct from the banks themselves, proved harder to secure.

The scandal confirmed what many had long suspected: that the benchmark-setting process for the world’s most traded asset class was, for years, systematically broken.

2. George Soros and Black Wednesday — Legal, But Market-Moving (1992)

Not every headline-making manipulation case results in a prosecution. Black Wednesday on September 16, 1992 is the most famous example.

The UK had joined the European Exchange Rate Mechanism in 1990 at a rate many economists considered unsustainably high for the domestic economy. George Soros, running Quantum Fund, concluded the same: the UK’s inflation was running at triple Germany’s rate, and maintaining the peg while defending it with interest rates was incompatible with the economic conditions. He built a $10 billion short position in sterling.

On September 16, the Bank of England spent billions of Deutsche Marks buying sterling to defend the floor. It failed. The government raised interest rates to 15% in a single day (10 percentage points in under 24 hours) to attract capital inflows. That failed too. By evening, sterling was pulled from the ERM and the pound devalued.

Soros’s profit: over £1 billion in a single day.

This wasn’t illegal in the conventional sense. No false information was spread. No orders were spoofed. Soros identified a structural mispricing created by government policy and positioned accordingly, at enormous scale. The UK Treasury’s official assessment put the cost to British taxpayers at £3.3 billion (revised estimate, 2005).

The debate about where aggressive speculation ends and manipulation begins never fully resolved. But Black Wednesday made clear that a single fund, with the right analysis and enough capital, can move a sovereign currency. That’s worth understanding even if no laws were broken.

3. The LIBOR Scandal — Barclays, Resignations, and the Rate That Moved Everything (2012)

LIBOR isn’t strictly a forex rate, but it’s inseparable from forex pricing. The London Interbank Offered Rate underpins interest rate differentials between currencies. That’s a foundational driver of forex valuations. When banks manipulated LIBOR, they moved currency markets.

Barclays was first to be exposed. Between January 2005 and June 2009, Barclays derivatives traders made 257 documented requests to fix LIBOR and EURIBOR submissions (CFTC, June 2012). They needed rates to fall on days they held short positions and to rise when long. They also asked their submitters directly, via email and instant message, often in casual, almost bored language.

There were two manipulation modes. During normal conditions, traders tilted submissions to benefit their derivatives books. During the 2008 financial crisis, submissions were deliberately lowered to make Barclays appear more creditworthy. That second motive, arguably, was worse: prioritizing institutional survival over market integrity.

On June 27, 2012, Barclays agreed to pay £290 million across three regulators: $200 million to the CFTC, $160 million to the DOJ, and £59.5 million to the UK Financial Services Authority. Chief Executive Bob Diamond resigned three days later. Chairman Marcus Agius had resigned the day before.

UBS followed in December 2012 with a $1.5 billion settlement. Deutsche Bank paid £227 million to the FCA in 2015 for LIBOR and EURIBOR manipulation running from 2005 through 2010. Total LIBOR settlements across all institutions exceeded $9 billion globally.

The scandal confirmed that rate benchmarks, presented to the world as objective market readings, had been editable by individuals with conflicting financial interests.

4. Tom Hayes — The First Trader Jailed for LIBOR (2015)

The banks paid. Individual traders took longer to prosecute.

Tom Hayes, a UBS yen derivatives trader, was the first person convicted by a UK jury for LIBOR manipulation. In August 2015, he was sentenced to 14 years in prison. On appeal, this was reduced to 11 years. He served just over five years before release on licence.

Hayes operated primarily in yen LIBOR; the rate used to price yen-denominated contracts globally. He built a network of contacts at other panel banks and brokerages, asking them to adjust their LIBOR submissions in exchange for directing business their way. He was explicit about it in his messages. There was no ambiguity about what he was doing or why.

His defense argued that LIBOR manipulation was standard industry practice, that his managers knew, that other banks knew, and that the entire system was designed to allow this kind of influence. There’s some evidence that argument has merit: in 2025, the UK Supreme Court overturned his conviction on the grounds that he was denied a fair trial. Hayes subsequently filed a $400 million lawsuit against UBS, alleging the bank used him as a scapegoat.

The legal twists don’t change what happened. He manipulated rates for years. The conviction, however imperfect, was the first time the financial system acknowledged that individuals; not just institutional entities, were criminally responsible.

5. Navinder Sarao and the 2010 Flash Crash — $40 Million from a Bedroom in Hounslow

On May 6, 2010, the Dow Jones Industrial Average dropped nearly 1,000 points in approximately 15 minutes, briefly erasing $1 trillion in market value before a partial recovery. It became known as the Flash Crash.

For five years, the cause was debated. In April 2015, the US Department of Justice arrested Navinder Sarao, a point-and-click trader operating from a semi-detached house in Hounslow, West London.

Sarao had modified a commercially available trading platform to layer four to six exceptionally large sell orders into the E-mini S&P 500 futures market simultaneously. His algorithm ensured these orders stayed three to four price levels away from the best ask: visible enough to distort the order book, never close enough to execute. The illusion of overwhelming sell pressure was the product. He’d cancel and re-enter the orders continuously, moving them dynamically to maintain the artificial pressure.

On May 6, 2010, he entered more than 85 large spoof orders, at times representing over 20% of all visible sell orders in the E-mini market (CFTC, 2015). The feedback loop triggered other algorithms and accelerated the crash.

Over four years using similar techniques, Sarao accumulated approximately $40 million in profits. He was not a sophisticated institutional player with access to inside information or market infrastructure. He was a retail trader who had reverse-engineered a loophole in the E-mini order book and used it for four years.

In January 2020, he was sentenced to one year of home confinement, no prison time, in recognition of his cooperation with authorities and his mental health circumstances.

The case was a turning point in how regulators thought about algorithmic manipulation. The Dodd-Frank Act had criminalized spoofing in 2010, the same year as the Flash Crash. Sarao’s case showed that the technology gap between retail and institutional participants created genuine systemic risk.

6. Michael Coscia — Dodd-Frank’s First Spoofing Conviction (2015)

Navinder Sarao attracted more headlines. Michael Coscia established the legal precedent.

In 2011, Coscia, founder of Panther Energy Trading in Red Bank, New Jersey, deployed an algorithm that placed large orders in CME futures markets, then canceled them within milliseconds. The algorithm was designed to move the price by a few ticks, execute smaller orders on the other side, then cancel before the large orders could actually fill. He ran this strategy across 6 different futures markets over just two months.

The CFTC and the UK’s Financial Conduct Authority both brought enforcement actions in 2013. Coscia paid $2.8 million to the CFTC and £903,000 to the FCA.

The criminal case came later. In November 2015, a federal jury in Chicago convicted him of six counts of commodities fraud and six counts of spoofing, the first criminal conviction under Dodd-Frank’s anti-spoofing provision. He was sentenced to three years in prison.

The Coscia case defined what spoofing means under US law and gave prosecutors a template for every spoofing case that followed, including JPMorgan’s $920 million settlement five years later.

7. JPMorgan’s Gold and Silver Spoofing Operation — Eight Years, $920 Million (2008–2020)

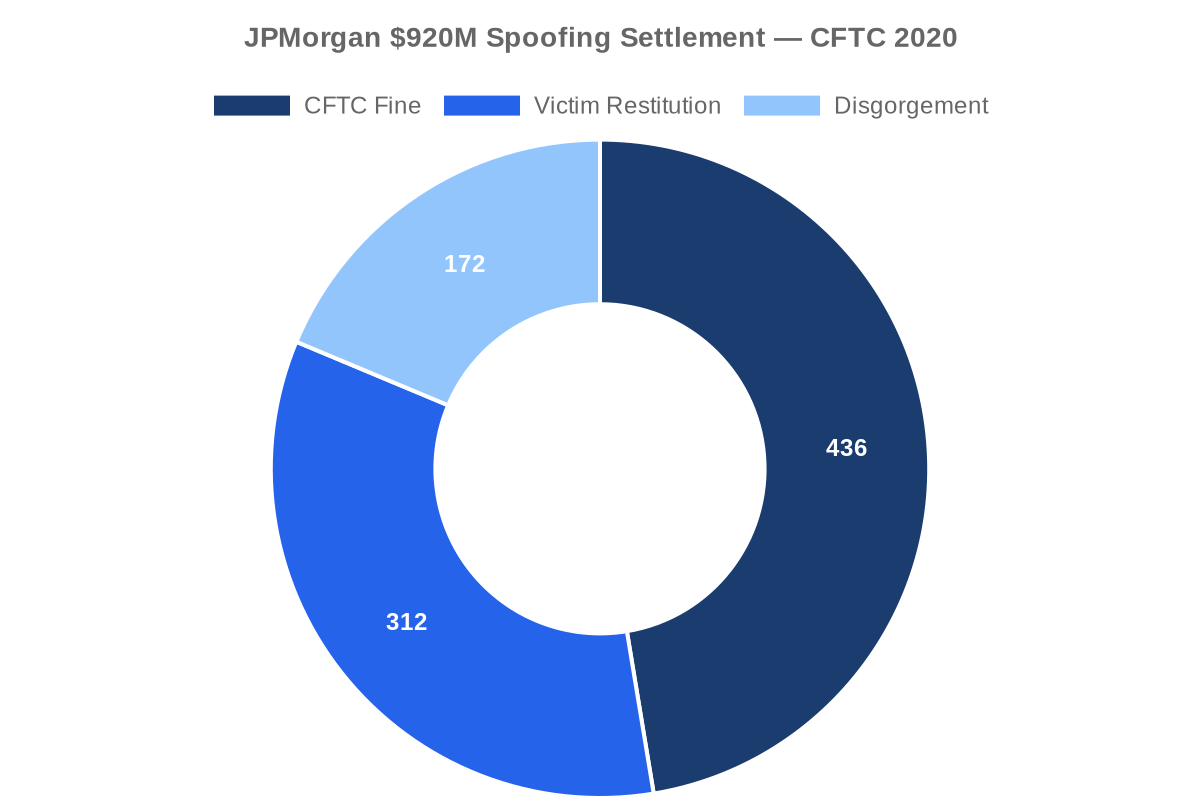

JPMorgan Chase admitted wrongdoing and agreed to pay $920.2 million in September 2020 to settle charges of systematic spoofing across precious metals and US Treasury markets. It was the largest spoofing penalty in CFTC history at the time.

The conduct ran from at least 2008 through 2016. Fifteen traders across JPMorgan’s metals and Treasury desks placed hundreds of thousands of orders to buy or sell gold, silver, platinum, palladium, Treasury notes, and Treasury bonds with the explicit intent to cancel before execution. The spoof orders created artificial signals of supply or demand, moving prices to benefit the smaller orders the traders actually wanted filled.

Total losses caused to other market participants: more than $300 million (CFTC, 2020).

Several individual traders faced criminal charges. The bank entered into a deferred prosecution agreement acknowledging that its traders committed fraud. The fine broke down as a $436.4 million CFTC penalty, $311.7 million in restitution to victims, and $172 million in disgorgement.

What makes this case notable beyond the fine amount: it covered eight years of misconduct at one of the most regulated, most scrutinized financial institutions in the world. Internal compliance reviews, regulatory examinations, and risk management processes all failed to identify or stop it.

8. HSBC Mark Johnson — Front-Running a $3.5 Billion Client Trade (2016–2017)

Front-running is market manipulation with a specific setup: you learn a client’s upcoming order, you position yourself ahead of it, and you profit from the price impact their own transaction creates.

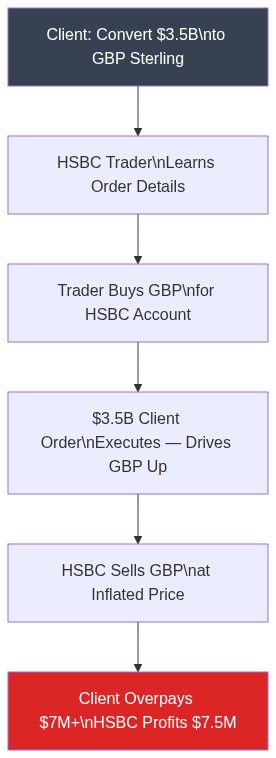

In 2011, HSBC was engaged to convert approximately $3.5 billion in sale proceeds into British pound sterling for a corporate client. Mark Johnson, HSBC’s global head of foreign exchange cash trading, directed traders to purchase sterling for HSBC’s proprietary accounts ahead of the client’s conversion.

When the $3.5 billion conversion executed; as Johnson knew it would, and roughly when, and in what currency, it drove up the price of sterling. HSBC’s pre-positioned accounts, now holding sterling bought at lower prices, profited from the move. HSBC generated approximately $7.5 million from the trade. The client overpaid by more than $7 million compared to the price available without the front-running.

Johnson was convicted by a federal jury in October 2017 of wire fraud conspiracy and eight counts of wire fraud. He was sentenced to 24 months in prison and fined $300,000.

This case matters to retail forex traders in a specific way. The mechanics of front-running scale down. Retail brokers with access to client order flow are not legally permitted to use that information for proprietary trading, but the structural temptation is identical to what Johnson acted on. Understanding how it works at the institutional level helps traders evaluate counterparty risk at the retail level.

9. The Swiss National Bank’s “Black Thursday” — When Central Bank Policy Becomes Market Shock (January 15, 2015)

Whether this qualifies as “manipulation” in the strict legal sense is genuinely debatable. Include it here because the outcome for traders was indistinguishable from the worst manipulation scenarios.

From 2011 through January 2015, the Swiss National Bank maintained a floor of 1.2000 on the EUR/CHF exchange rate. The peg was explicit: the SNB would buy unlimited euros to prevent the franc from strengthening beyond that level. For three years, traders and institutions positioned accordingly. The floor was treated as a known, defended line.

On January 15, 2015, the SNB removed the peg without warning. EUR/CHF fell from 1.2000 to a low near 0.9650 within minutes: a move of more than 20% in a currency pair that typically moves 0.5% on an eventful day. CHF/USD moved similarly. Brokers including FXCM reported losses exceeding their net capital. Several retail brokers went insolvent. Traders who had been long EUR/CHF based on the SNB’s stated policy were wiped out before stop-losses could execute at any reasonable price.

I’ve spoken with traders who were long EUR/CHF that morning on the assumption the floor was permanent. None of them got filled near their stop. It reshaped how I think about ‘guaranteed’ policy levels.

The SNB’s defense was straightforward: the peg was a policy tool, not a contractual guarantee. Central banks can change policy. They have no obligation to pre-announce.

That’s legally correct. But the market outcome was identical to a coordinated manipulation event: a sudden, extreme price move that transferred wealth from one group to another, with zero advance notice. Switzerland was subsequently added to the US Treasury’s currency manipulator watchlist for its ongoing FX interventions.

10. Telegram Pump-and-Dump Groups — Manipulation at Scale, Without the Bankers (2018–Present)

The first nine examples involve institutional actors, major banks, and regulatory enforcement. This one doesn’t.

Since roughly 2018, coordinated pump-and-dump operations have moved from penny stocks (the traditional venue) to thinly traded currency pairs, cryptocurrency tokens, and retail CFD products. The mechanism is the same, the technology is different. A group of participants coordinate via encrypted messaging (Telegram, Discord), agree on a target asset, simultaneously buy to drive up the price, then signal followers to buy in as well. Once the price has risen sufficiently, the original coordinators sell into the inflated demand and exit.

In crypto markets, manipulators generated $241.6 million in verified pump-and-dump profits in 2023 alone, primarily through decentralized exchange tokens (Chainalysis, 2023). While not directly forex, the same structural vulnerabilities exist in foreign and illiquid currency pair markets — particularly those accessible via unregulated CFD brokers.

For retail traders in any market, the risk isn’t abstract. Joining a “signal group” that promises advance notice of price movements should be treated as a strong indicator of participation in illegal activity — regardless of how the group presents itself.

How to Protect Yourself From Market Manipulation

Knowing these cases happened isn’t enough on its own. Four practices reduce your actual exposure.

- Trade through regulated brokers. FCA (UK), ASIC (Australia), CySEC (EU), and NFA (US) all enforce conduct standards that, while imperfect, significantly reduce broker-level manipulation risk. Unregulated brokers operate with no external oversight of their price feeds, order routing, or execution practices.

- Avoid benchmark-window periods. The WM/Reuters fix at 4:00 PM London time was the specific target of the 2013 manipulation. Trading during major benchmark windows and significant economic releases means trading when incentives for manipulation are highest.

- Use limit orders. Stop-loss orders — particularly in illiquid market conditions — are execution promises the broker can fill at any price once the stop is triggered. Limit orders cap your entry and exit prices. You may miss trades, but you won’t be filled at 20% away from your intended level.

- Be skeptical of “signal groups.” Pre-announced price movements don’t come from analysis. They come from coordinated positioning. If someone knows a currency pair is about to move, they’ve either manipulated it or received inside information — neither of which is a service you want to participate in.

Conclusion

The forex market’s $7.5 trillion daily turnover offers no protection against manipulation, if anything, its scale and predictability invite it. From the FX Cartel rigging benchmark rates to lone traders spoofing order books from a bedroom, the ten cases here share one logic: manufacture a false price signal, then trade against it. Regulators have responded with record fines and prison sentences, yet enforcement always trails the conduct. For retail traders, the practical defence is unglamorous but effective: choose regulated brokers, avoid benchmark windows, use limit orders, and treat any “signal group” as a red flag. Awareness remains your strongest position.

Frequently Asked Questions

1. What is market manipulation in simple terms?

Market manipulation is any deliberate attempt to artificially move an asset’s price through deceptive means — fake orders, coordinated buying or selling, false information, or exploitation of confidential client data — to profit at the expense of other market participants.

2. What is the difference between market manipulation and insider trading?

These terms overlap but aren’t identical. Market manipulation involves artificially moving prices through deceptive means. Insider trading is the use of material, non-public information to make profitable trades. HSBC’s Mark Johnson case combined both: he used confidential client information (insider element) to front-run a trade that moved the market in his favor (manipulation element). Both are illegal; both are treated as serious criminal offenses in the US and UK.

3. Can the forex market really be manipulated given its size?

The $7.5 trillion daily volume doesn’t protect against manipulation at benchmark windows, in specific currency pairs, or at the retail broker level. The 2013 FX scandal showed that even the world’s largest market is vulnerable when participants with concentrated market power coordinate their activity across a narrow, predictable time window. Six banks colluded on the WM/Reuters fix for years. Size and liquidity are not immunity from manipulation — they just change the scale at which it needs to operate.

4. What is price manipulation in forex?

Price manipulation in forex refers to any deliberate interference with a currency pair’s exchange rate through artificial means: spoofing order books to create false supply or demand signals, front-running large client orders, coordinating benchmark rate submissions, or using algorithmic tools to create misleading price patterns.

5. Has anyone been sent to prison for forex market manipulation?

Yes. Mark Johnson (HSBC) served 24 months for front-running a $3.5 billion client trade. Tom Hayes (UBS) served more than five years for LIBOR manipulation, though his conviction was overturned in 2025 on procedural grounds. Michael Coscia served three years for spoofing under the Dodd-Frank Act. Several traders connected to the broader 2013 FX and LIBOR scandals faced criminal charges and convictions, though most were at the individual rather than institutional level.