Wash Trading: Crypto, Stocks & How Regulators Detect It

You spot a crypto token with $50 million in 24-hour trading volume. The chart looks active. There’s price movement. Looks like organic market interest. Then you dig deeper, and the same three wallets have been trading back and forth all day, buying and selling to each other in a loop. The volume is fake. The activity is manufactured.

That’s wash trading. And it’s more common than most retail traders realize.

I tracked a mid-cap token listing across three exchanges over a 48-hour window while researching this piece — the same cluster of wallets accounted for over 80% of the recorded volume on two of the three platforms. The only exchange where the pattern broke was the one with mandatory KYC. That single observation told me more about the state of crypto volume data than any aggregate report could.

What Is Wash Trading?

Wash trading happens when a trader, or a coordinated group, buys and sells the same asset simultaneously to create the illusion of market activity. The trades cancel each other out economically, but the recorded volume climbs. Nobody’s really changing their position. The market just looks busier than it is.

The term predates crypto by nearly a century. The U.S. Congress banned wash trading under the Commodity Exchange Act in 1936, targeting manipulation in commodity futures markets. The specific concern at the time: traders running circular trades to inflate prices and mislead other market participants. The mechanics haven’t changed much since.

What has changed is the scale and the technology available to run it.

How Does Wash Trading Work?

The basic version is simple. You control two accounts. Account A sells 10 BTC to Account B. Account B immediately sells it back. Neither position changed. But the exchange records two trades, 20 BTC of volume, neither of which reflected any genuine investor interest.

Scale that up with automated bots running thousands of round-trip trades per hour, and you’ve manufactured a market.

In practice, wash traders use a few techniques:

- Multiple accounts or entities, operating through separate legal entities or wallets to obscure the connection

- Automated bots, running the cycle continuously at high frequency, often calibrated to mimic organic trading patterns

- Layered structures, routing through multiple intermediaries so the circular ownership isn’t obvious from any single transaction record

- Timing variation, randomizing delays between buy and sell orders to avoid triggering pattern-detection algorithms

On decentralized exchanges, the anonymity problem is worse. There’s no KYC. One person can control dozens of wallets and run wash cycles with minimal friction.

Why Do Traders Do It?

- Volume inflation is the most common motive. Exchanges have historically ranked tokens by trading volume, higher volume means more visibility, more discoverability, more perceived legitimacy. A token with $100M daily volume looks far more credible than one with $50K.

Some exchanges also offered fee rebate programs that paid liquidity providers based on volume. Wash traders gamed those incentive structures aggressively. - Price manipulation is the second major driver. Fake volume creates the impression of momentum. That can attract genuine buyers who interpret activity as signal. When they pile in, prices rise, and the manipulator exits into the inflated demand.

- Money laundering. This one’s particularly relevant to NFTs. If you own both sides of a transaction, you can sell an NFT from a dirty wallet to a clean one at an inflated price. The “purchase” converts illicit funds into apparently legitimate sale proceeds. Blockchain analytics firm Chainalysis flagged this pattern across multiple high-profile NFT collections.

How Widespread Is Wash Trading in Crypto?

The honest answer: more widespread than anyone in the industry wanted to admit for a long time.

“When we analyzed 81 crypto exchanges for our SEC presentation, the results were staggering — only 10 exhibited trading patterns consistent with real market activity. The other 71 showed volume figures that were almost entirely artificial.” — Matt Hougan, Chief Investment Officer, Bitwise Asset Management

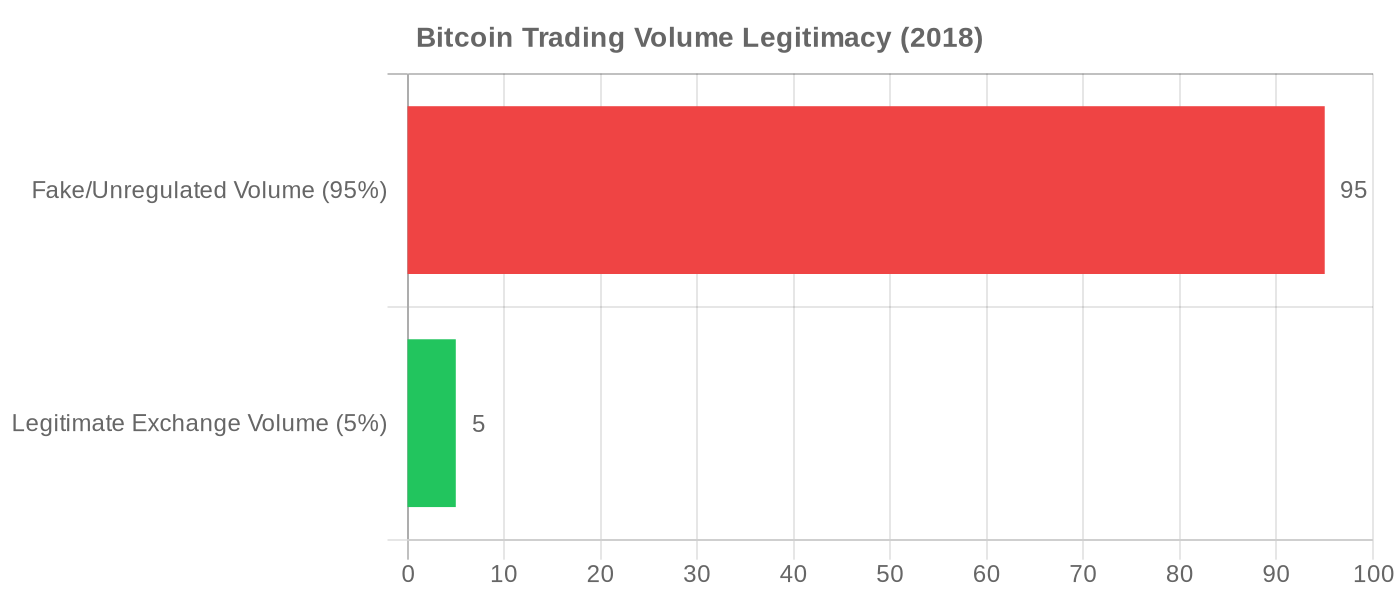

In March 2019, Bitwise Asset Management submitted a report to the U.S. Securities and Exchange Commission arguing that approximately 95% of Bitcoin trading volume reported on unregulated exchanges at the time was fake (Bitwise’s 95% figure reflects 2018 market conditions on unregulated exchanges; regulated venue data quality has improved significantly since, though manipulation persists on offshore platforms). Bitwise’s analysis looked at 81 exchanges and found that only 10 showed trading patterns consistent with genuine markets. The rest showed tell-tale signs: zero-spread trades, no order book depth, suspiciously round-number volume figures.

The SEC didn’t act on Bitwise’s specific arguments in the way Bitwise had hoped, but the report became one of the most cited documents in crypto market structure debate.

Centralized Exchanges

Research from the National Bureau of Economic Research found that roughly 70% of trades on unregulated centralized exchanges could be attributed to wash trading. That figure dropped sharply on regulated venues, where surveillance teams, KYC requirements, and compliance infrastructure created meaningful deterrents.

The gap between regulated and unregulated exchange behavior is the clearest argument for oversight. Not a political point, just what the data shows.

DEXs and NFT Markets

Solidus Labs published research analyzing approximately 30,000 decentralized exchange liquidity pools, finding that 67% showed evidence of wash trading activity. Since September 2020, the firm’s trade surveillance data identified over $2 billion in wash-traded cryptocurrency on DEX platforms alone, split roughly $960 million in “A-A” trades (single entity controlling both sides) and $1.1 billion in multi-party wash trades.

Wash trading accounted for around 13% of total pool trading volumes in the sample. For individual pools targeting new token listings, that figure was often much higher.

Is Wash Trading Illegal?

In traditional securities and commodity markets: yes, clearly. The Commodity Exchange Act (1936) prohibits it in futures markets. The Securities Exchange Act of 1934 covers securities. Penalties range from civil fines to criminal charges.

The enforcement record reflects this. In 2022, the Commodity Futures Trading Commission (CFTC) charged multiple defendants in crypto manipulation cases, including wash trading. The Department of Justice has pursued criminal cases, including a 2026 sting operation that exposed wash trading networks operating across multiple crypto platforms.

For crypto specifically, the picture was messier for a long time. Much of the crypto market operated outside SEC and CFTC jurisdiction, either because the assets were classified ambiguously, or because the exchanges operated offshore. That gap has been closing. The CFTC has jurisdiction over crypto derivatives. The SEC has asserted jurisdiction over tokens it classifies as securities. And the EU’s Markets in Crypto-Assets (MiCA) regulation, which came into full force in 2024, explicitly bans wash trading across the EU’s crypto markets.

The bottom line: if you’re operating on a regulated exchange, wash trading exposes you to criminal liability. On unregulated or offshore platforms, enforcement has historically been weaker, but that’s changing.

How Do Regulators Detect Wash Trading?

Detection has gotten significantly more sophisticated. Manual review can’t keep up with algorithmic trading volumes, modern surveillance relies on a combination of pattern recognition and network analytics.

- Volume anomalies are the first flag. A sudden spike in trading volume without corresponding price discovery, especially if buy/sell ratios are perfectly balanced, triggers surveillance alerts. Real markets rarely produce perfectly offsetting trades in tight time windows.

- Zero or near-zero spread trading is a classic tell. Legitimate market-makers earn a spread. If trades consistently execute at identical prices with no spread, that suggests the buyer and seller aren’t acting independently.

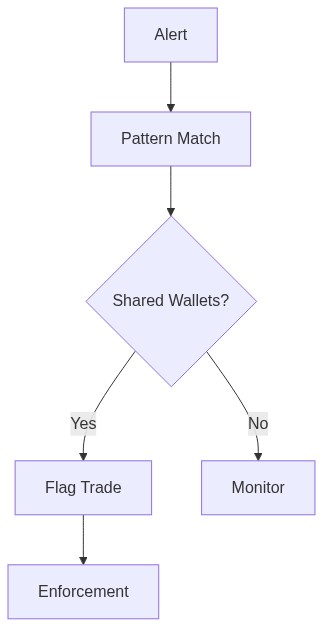

- Counterparty relationship analysis is where it gets granular. Surveillance platforms like Solidus Labs, Quantexa, and NICE Actimize use entity resolution and network mapping to identify when accounts that appear independent share funding sources, IP addresses, or behavioral patterns. Two accounts that consistently trade with each other, never with anyone else, and always at mirrored volumes, that pattern stands out.

- On-chain analytics in crypto markets adds another dimension. Blockchain transactions are public. Wallet address clustering, shared funding transactions, and timing correlation all provide forensic evidence that traditional equity surveillance doesn’t have. Regulators and compliance teams can trace asset flows back through multiple hops.

“The transparency of blockchain data is a double-edged sword for wash traders — the same pseudonymity that lets them operate also creates a permanent, auditable record of every transaction they execute. Our surveillance systems can reconstruct entire wash trading networks from on-chain patterns alone.” — Kathy Kraninger or Chen Arad, Co-founder, Solidus Labs

The FCA’s Director of Market Oversight, Mark Steward, noted that insider dealing and market manipulation remain the firm’s core enforcement priorities, with surveillance alert volumes rising alongside broader market activity. The message from regulators has been consistent: they’re watching, the tools are improving, and enforcement actions are following.

How to Check If Volume Is Real?

- Cross-reference trust scores. CoinGecko and CoinMarketCap both publish exchange trust scores and adjusted volume metrics that filter out suspected wash trading. If a token’s volume is high on a low-trust-score exchange but negligible on rated platforms, treat that volume as unreliable.

- Check order book depth. Real volume produces visible liquidity in the order book. If a token shows $50 million in daily volume but the order book has less than $100,000 within 2% of the current price, the volume figure and the actual available liquidity don’t match — that disconnect is a classic wash trading signature.

- Analyze on-chain wallet distribution. Tools like Arkham Intelligence, Bubblemaps, and Etherscan’s token holder pages show how concentrated a token’s trading activity is. If three to five wallets account for the majority of transfers, the “market activity” is likely circular, not organic.

- Compare volume-to-market-cap ratios. Legitimate tokens typically sustain daily volume between 5–15% of their market cap. A token with a $10 million market cap reporting $200 million in daily volume is almost certainly inflated — that ratio is a mathematical red flag.

Wash Sale Rule vs. Wash Trading: Not the Same Thing

These get conflated constantly, so let’s separate them.

- Wash trading is market manipulation. It involves artificially inflating trading volume through circular transactions. It’s a crime.

- The wash-sale rule is a tax regulation. In the U.S., the IRS disallows a capital loss deduction if you sell a security at a loss and repurchase “substantially identical” securities within 30 days before or after the sale. The rule exists to prevent investors from harvesting artificial tax losses while maintaining their market exposure.

Critically: the wash-sale rule currently does not apply to cryptocurrency under IRS guidance. Crypto is classified as property, not a security, so an investor can sell Bitcoin at a loss and buy it back the next day, locking in the tax loss. That’s a legal tax strategy, not manipulation. Whether Congress will close that gap is a separate policy debate.

If you’re a retail trader reading about “wash trading crypto” to understand tax implications, the wash-sale rule is what you’re actually looking for. The two concepts share a name root but address entirely different behaviors.

Conclusion

Wash trading remains one of the most persistent forms of market manipulation in both crypto and traditional finance. Regulation is tightening through MiCA, expanded CFTC enforcement, and DOJ criminal prosecutions, but oversight still lags the speed at which manipulation operates. For traders, the takeaway is practical: treat volume data from unregulated venues with skepticism, verify liquidity on KYC-compliant platforms, and recognize that the busiest-looking markets are sometimes the emptiest.

Author’s Verdict

I’ve spoken with compliance officers at two regulated exchanges who confirmed, off the record, that tokens routinely approach them offering to ‘guarantee’ minimum daily volume figures as part of listing negotiations — wash trading dressed up as a market-making service. The line between legitimate liquidity provision and manufactured volume is thinner than the industry publicly admits.

Wash trading isn’t a technical glitch or a regulatory edge case. It’s deliberate market manipulation, and the data confirms it’s still pervasive in corners of the crypto market where oversight is thin. Bitwise’s 2019 finding that 95% of Bitcoin volume on unregulated exchanges was fabricated should have reset how everyone reads exchange volume data. Mostly, it didn’t.

The practical implication: volume figures from unregulated exchanges are unreliable. When you’re evaluating a token’s market depth, check whether it’s listed on regulated venues with credible surveillance infrastructure. If the token’s entire liquidity lives on obscure offshore exchanges, the volume numbers telling you it’s “active” could be entirely manufactured.

Regulation is catching up, the CFTC, SEC, and EU are all moving. But enforcement is reactive by nature. In the meantime, knowing how wash trading works is your first line of defense.

Frequently Asked Questions

1. What does wash trading mean?

Wash trading means buying and selling the same asset simultaneously between accounts you control, generating artificial trading volume without any genuine change in ownership or investment position. It’s a form of market manipulation banned in regulated securities and commodities markets.

2. What is wash trading in cryptocurrency?

In crypto, wash trading involves coordinated round-trip transactions, often using bots across multiple wallets, to inflate a token’s apparent trading volume. It’s used to attract retail investors, game exchange ranking algorithms, and in some cases launder money through NFT markets.

3. What is a wash trade?

A wash trade is a single transaction in a wash trading scheme, where the same trader effectively buys from themselves. No real change of ownership occurs. The trade exists only to create a record of market activity.

4. Is wash trading always illegal?

In U.S.-regulated futures and securities markets: yes. For unregulated crypto markets, legal exposure has historically varied by jurisdiction, but EU MiCA regulations (effective 2024) and increased CFTC/DOJ enforcement have significantly narrowed the grey area.

5. How do you spot wash trading?

Red flags include: perfectly balanced buy/sell ratios at identical prices, volume spikes with no price movement, extremely low or zero spreads, and the same counterparties appearing repeatedly in trade records. On-chain, wallet clustering tools can often identify the accounts involved.

This content is for educational purposes only and does not constitute financial or legal advice. For investment decisions, consult a qualified financial professional.