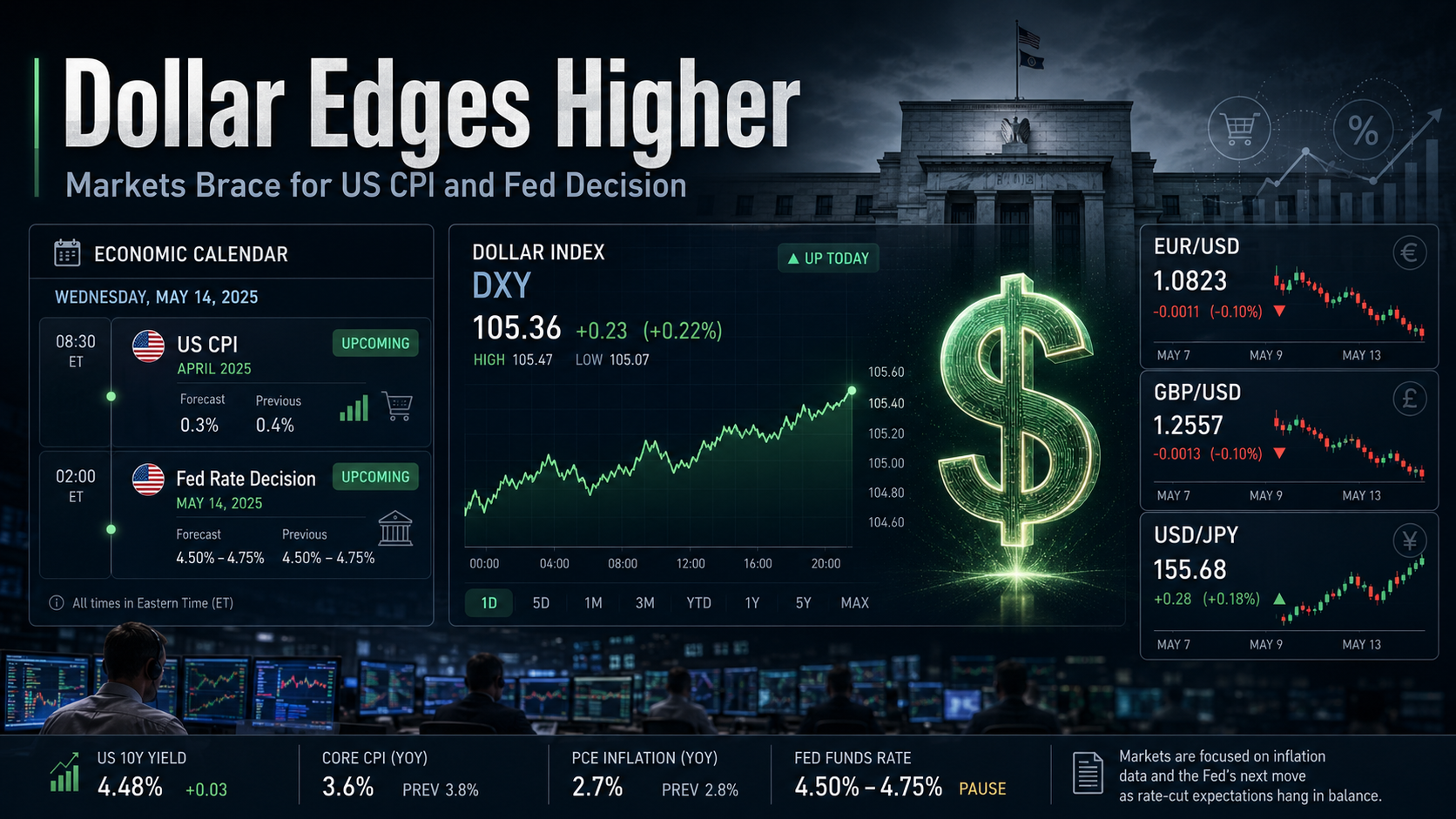

The US dollar firmed against major currencies on Monday as foreign exchange markets positioned for a week that could reshape rate-cut expectations for the rest of 2026.

Two releases dominate the calendar: the latest US Consumer Price Index (CPI) report and the Federal Reserve’s policy decision. Both land this week. Both carry enough weight to move every dollar pair on the board.

Why This Week Matters for the Dollar

Traders aren’t watching one data point. They’re watching whether the inflation picture has shifted enough for the Fed to signal anything new.

Sticky inflation has kept the Federal Reserve cautious for months. Rate-cut expectations have been pushed back repeatedly since January, and the dollar has strengthened each time the timeline extended. If CPI comes in hot again, that trade gets reinforced. A cooler reading opens the door to a different conversation entirely.

The sequencing matters here. CPI drops before the Fed announces, which means the committee will have fresh inflation data in hand when they release their statement and updated projections. Markets will parse every line for hints about whether the number moved anyone on the committee.

Dollar Strength Built on Rate Differentials

The greenback’s firmness isn’t happening in isolation. Rate differentials continue to favor the dollar over most G10 peers — the euro, the pound, and the commodity currencies have all struggled to sustain rallies against it.

That gap persists for a simple reason. The Fed stays on hold while other central banks have already started cutting or signaled they’re close. The European Central Bank (ECB) has eased. The Bank of England (BOE) has eased. The Fed hasn’t. As long as that’s the case, the dollar earns a carry premium that’s hard to trade against.

Plain and simple: yield advantage is the dollar’s backstop right now.

Yen Under Pressure Near Intervention Watch Levels

The Japanese yen remains the weakest major currency in the G10. It’s trading near levels that have historically triggered intervention warnings from Tokyo.

The Bank of Japan (BOJ) is the outlier among central banks. While everyone else debates how fast to cut, the BOJ is still working out how fast to normalize from decades of ultra-loose policy. “Very gradual” is the phrase that keeps coming up — and the market keeps testing that patience.

Japanese officials follow a pattern. Verbal warnings first. Actual intervention if the yen blows past their pain threshold. Traders who were around for the 2022 and 2024 episodes know what happens: the yen grinds weaker for weeks, everyone ignores the warnings, then the Ministry of Finance steps in and the pair snaps back in a single session.

Not a comfortable position to hold if you’re on the wrong side.

Options Markets Price In Bigger Moves

Volatility expectations across dollar pairs are elevated heading into the week, according to Reuters. That’s rational. CPI alone moves markets. A Fed decision alone moves markets. Both in the same week means hedging costs climb and position sizes shrink.

The practical effect on Monday: wider spreads, thinner liquidity, and a market that’s leaning cautiously dollar-long while it waits. Nobody’s making bold bets ahead of the data.

Analyst Take

The dollar’s bid heading into this week is more about positioning than conviction. Being short dollars into a CPI print that could surprise to the upside, followed by a Fed that has shown zero urgency to cut — that’s not a risk most desks want to carry.

The yen side is more interesting. BOJ gradualism has created what looks like a one-way bet, and everyone knows it reverses eventually. The question is whether it reverses on the BOJ’s terms or on the Ministry of Finance’s terms. Either way, the snapback tends to be sharp.

If CPI comes in soft and the Fed hints at a September move, the dollar gives back this week’s gains by Friday. If inflation stays stubborn, the higher-for-longer trade extends and yen intervention risk ratchets up another notch.

What to Watch This Week

- US CPI release — the inflation print that drops before the Fed decision, setting the tone for market expectations

- Federal Reserve policy statement — the rate decision, updated dot plot, and economic projections will signal the committee’s rate path

- BOJ commentary — any language shift on yen weakness or willingness to act

- USD/JPY price action — the pair most likely to move on intervention signals