Iran War Fuels Forex Chaos Ahead of Central Bank Week

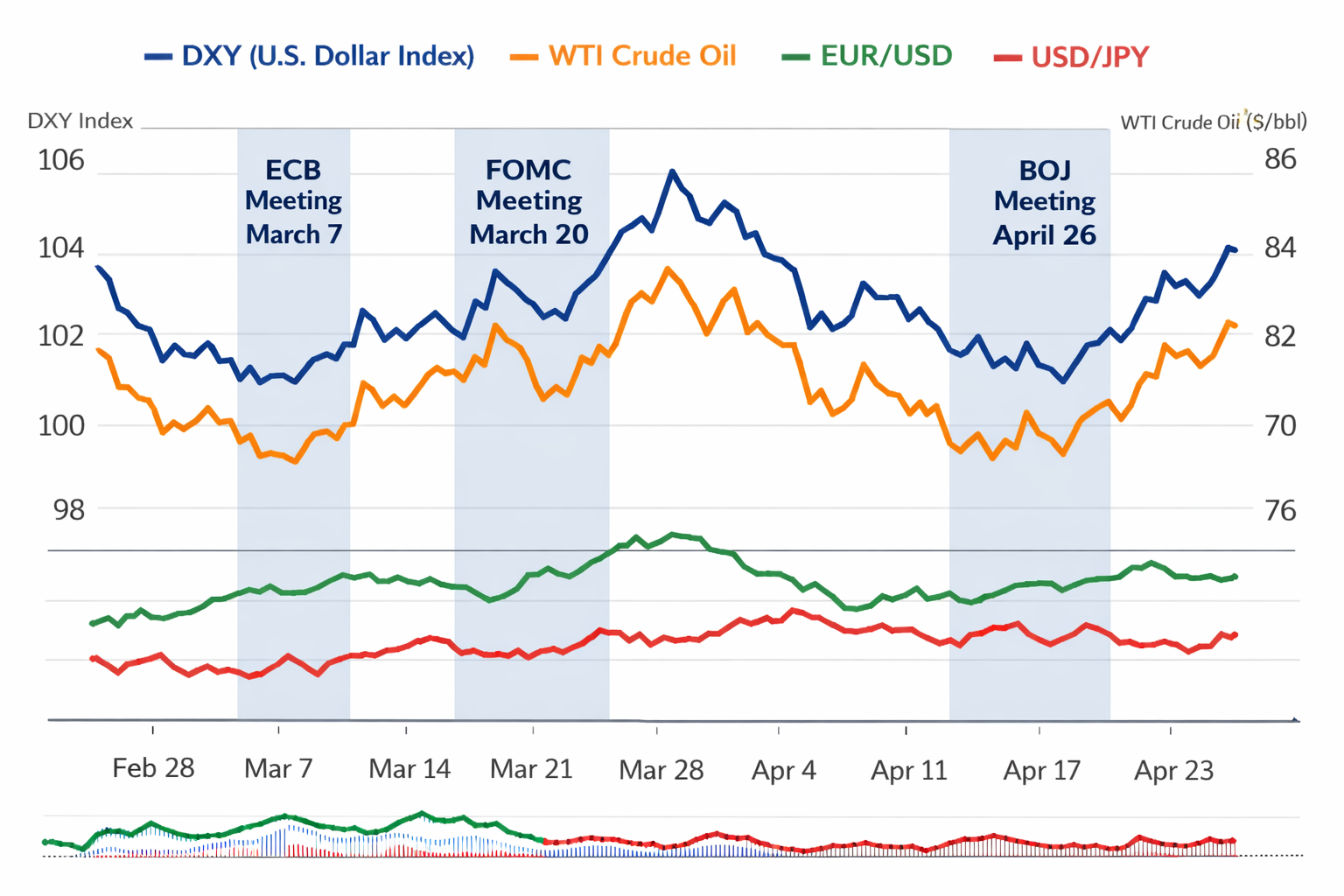

Geopolitical tensions stemming from the US-Israel strikes on Iran since February 28, 2026, have unleashed volatility across global forex markets. Oil prices are hovering near $100 per barrel, while the US Dollar Index (DXY) has surged to 99. This week, policy decisions from seven major central banks—including the Federal Reserve, European Central Bank, and Bank of Japan—could further shift currency dynamics amid energy shocks and rising inflation concerns.

Traders now face a high-stakes environment combining safe-haven flows, commodity price pressures, and uncertainty around monetary policy.

Iran Conflict Triggers Energy Supply Fears

The Strait of Hormuz, which handles roughly 20% of global oil and LNG shipments, remains a critical flashpoint after Iran threatened to close the route. Brent crude surged from $85 to peaks near $119 before stabilizing between $100 and $105.

Key impacts on currency markets include:

- Safe-haven dollar rally: The US Dollar Index climbed from 96 to 99, supported by oil’s dollar pricing and strong global demand for US liquidity.

- Euro weakness: EUR/USD dropped toward 1.1417 as Europe faces lower gas reserves and higher energy import dependence.

- Mixed performance for petrocurrencies: Despite higher oil prices, the Canadian dollar remains under pressure as broader risk-off sentiment favors the US dollar.

Several countries, including Australia, have rejected naval coalition proposals to secure the Strait of Hormuz, increasing concerns about future supply disruptions.

Safe-Haven Shifts: Dollar Strong While Yen and Franc Face Limits

Traditional safe-haven assets are showing unusual behavior during the crisis. While the US dollar has strengthened on higher yields and energy advantages, other safe havens face policy constraints.

- Swiss franc: USD/CHF near 0.7890, with the Swiss National Bank warning it may intervene to prevent excessive currency appreciation.

- Japanese yen: USD/JPY has climbed above 159 due to yield differentials and expectations that the Bank of Japan will hold policy steady. Markets view 160 as a potential intervention threshold.

Gold has fluctuated around $5,000 despite geopolitical risks, reflecting strong demand for dollar liquidity rather than traditional inflation hedges. Meanwhile, the British pound has held relatively firm amid expectations of a more hawkish Bank of England stance.

Central Bank Week: Holds, Hikes, and Hawkish Repricing

Seven major central banks are scheduled to announce policy decisions between March 16 and March 19, significantly altering expectations for global interest rate cuts in 2026.

| Central Bank | Expected Action | Key Forex Impact |

|---|---|---|

| RBA (Mar 17) | 25 basis point hike to 4.10% | AUD/USD could move toward 0.7189 |

| Fed (Mar 18) | Hold at 3.50–3.75% | Rate cuts likely delayed to December |

| BoC (Mar 18) | Hold at 2.25% | CAD pressured by weaker jobs data |

| BoJ (Mar 18–19) | Hold policy | Continued risk of yen intervention |

| BoE / ECB / SNB | Likely policy holds | Potential divergence in EUR and GBP performance |

Major financial institutions including Goldman Sachs and Barclays now expect rate cuts to be delayed until September or later. Meanwhile, US consumer sentiment has fallen to 55.5, while inflation expectations remain elevated at 3.4%.

Emerging Markets Under Pressure

Energy-importing economies are particularly vulnerable to the oil shock.

- Indian rupee: Reached a record low of 92.43 per US dollar, with risks of moving toward 95 as oil import costs rise.

- South Korean won: Approaching 1,500 per US dollar amid global risk aversion.

China’s stronger economic data, including a 6.3% rise in industrial production, has provided limited support to regional currencies. Meanwhile, Bitcoin has remained resilient, holding above $73,000 as some investors treat it as an alternative safe-haven asset.

Market Impacts and Potential Trade Setups

- EUR/USD: Key support around 1.1590, with RSI above 60 indicating potential downside risks.

- USD/JPY: Uptrend channel remains intact toward 160, though policy intervention could cap gains.

- AUD/USD: Pullbacks toward 0.6900 may present buying opportunities.

More broadly, delayed rate cuts are supporting global bond yields, increasing pressure on emerging market currencies. Rising oil prices are also slowing the disinflation trend that central banks had hoped would allow easier monetary policy.

Outlook

Forex traders are closely monitoring intervention risks, trading ranges, and central bank policy signals. A resolution to tensions around the Strait of Hormuz or unexpectedly dovish policy decisions could weaken the US dollar. However, further escalation would likely reinforce demand for the dollar as the dominant global safe-haven currency.

Key events to watch include the Federal Reserve’s updated economic projections and the Bank of Japan’s policy statement.

Alexandra Winters’ Take:

This perfect storm of Iran risks and central bank holds could lock DXY above 99 short-term, squeezing EM currencies further, but a Hormuz de-escalation or Fed dovishness might spark rapid reversals—traders should size small, eye 160 on USD/JPY for interventions, and favor yield plays like AUD until clarity emerges.