Iran Conflict Sparks Dollar Rally, Oil Surge

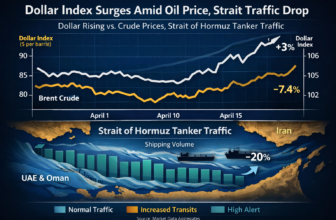

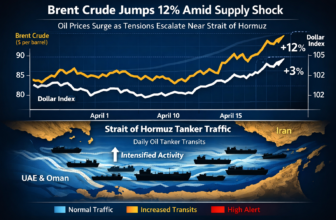

The U.S. and Israeli military operations against Iran, culminating in the reported death of Supreme Leader Ali Khamenei on February 28, have triggered a dramatic reassessment of geopolitical risk across forex and commodity markets. The subsequent closure of the Strait of Hormuz—the world’s most critical maritime chokepoint—has created an unprecedented supply shock, with oil prices surging toward $80–84 per barrel as traders grapple with disruptions affecting approximately 20% of global oil supplies.

The Islamic Revolutionary Guard Corps declared the Strait a closed military zone on March 2, fundamentally altering shipping infrastructure and forcing tankers to reroute around the Cape of Good Hope—adding 10–14 days to delivery times and quadrupling operating costs to approximately $425,000 per day. This logistical nightmare has left nearly 1,000 vessels idling near the Strait, representing approximately $25 billion in vessel value alone, while Iraq has been forced to slash production by 1.5 million barrels per day due to lack of viable export routes.

The Dollar’s Complex Safe-Haven Response

The U.S. Dollar has experienced renewed strength, with the USD Index (DXY) rising approximately 1.5% in early-week trading, though analysts caution that this movement has been driven substantially by short-position covering rather than genuine safe-haven flows. By March 5, the DXY traded near 99.50 resistance levels, supported by safe-haven flows as geopolitical fears intensified.

Initial market reactions were nuanced: equity markets initially rallied on March 4, with the NASDAQ gaining 1.4% and the S&P 500 rising nearly 1%, suggesting investors viewed U.S. military capabilities as sufficient to contain the conflict. However, this risk-on sentiment reversed sharply by March 5–6 as geopolitical uncertainty deepened.

The dollar strengthened most sharply against commodity-linked currencies, with the greenback gaining 1.31% versus the Australian Dollar on March 5 as risk-off sentiment overwhelmed commodity-price support. This divergence highlights a critical tension: while elevated oil prices theoretically support commodity currencies, geopolitical risk premia have dominated actual trading dynamics.

Euro and Sterling Under Pressure Despite Structural Support

The EUR/USD pair has extended its weekly slide, touching its lowest level since late November below 1.1550 on March 4, before consolidating above 1.1600 by March 5–6. The euro’s weakness persists despite structural rationale for strength, as the ECB’s “persistent uncertainty” rhetoric has prevented meaningful decoupling from U.S. Dollar strength.

Technical analysts have identified critical support at 1.1578, with a bearish case suggesting deeper slides toward 1.1500 if this level breaks. Conversely, reclaiming the 200-day moving average near 1.1670 would signal the broader uptrend remains intact and could trigger a wave of technical buying back toward 1.1800.

The British Pound has experienced similar pressure, with GBP/USD stabilizing around 1.3350 following a two-day slide, as traders monitor the year-to-date low of 1.3340 as a critical support level. The broader risk-off sentiment has overwhelmed expectations of an imminent Bank of England rate cut, with unemployment recently hitting a new high of 5.2%—just short of the COVID peak of 5.3%.

Australian Dollar Collapses; Commodity Currencies Battered

The Australian Dollar has borne the brunt of risk-off positioning, with AUD/USD falling sharply to the 0.6990 price zone on March 5. The pair has erased most of the week’s early gains, with price continuing to consolidate within a roughly 150-pip band between 0.7000 and year-to-date highs near 0.7150. While bulls may initially look to buy dips toward mid-0.6900s support, the established uptrend faces significant headwinds from geopolitical uncertainty.

The Japanese Yen has also experienced pressure, with USD/JPY correcting lower and trading below 157.50 after rising for two straight days, reflecting competing pressures between rising oil prices (supportive of USD) and potential safe-haven flows.

Labor Market Mixed Signals Ahead of Critical Payrolls Release

Recent employment data has painted a deeply mixed picture heading into Friday’s critical nonfarm payrolls release at 8:30 AM ET. The Challenger Job Cuts report showed U.S. employers announced just 48,307 job cuts in February—down 55% from January’s 108,435, suggesting moderating restructuring efforts. More significantly, initial jobless claims remained unchanged at 213,000, coming in below the 215,000 forecast and reinforcing a “low-hire, low-fire” labor market environment.

However, the broader employment picture reveals underlying weakness. January’s surprise 130,000 nonfarm payroll gain masked substantial internal deterioration, with revisions revealing 862,000 fewer jobs created over the 12 months through March 2025, concentrated in healthcare and social assistance.

Market consensus expects modest deceleration to 59,000–60,000 jobs for March, with unemployment expected to hold steady at 4.3% and average hourly earnings projected at 3.7% annual growth. This wage growth rate represents the “danger zone” for potential stagflation concerns if combined with persistently elevated oil prices.

Fed Policy Transition Adds to Uncertainty

The White House’s nomination of Kevin Warsh as the next Federal Reserve Chair has created significant market uncertainty, with initial reactions reflecting both hawkish and dovish interpretations of his monetary policy stance. Interest rate futures have repriced to reflect only two 0.25% rate cuts in 2026, down from three expected in the prior week.

Warsh’s track record presents a complex picture: he opposed rate cuts during the 2008 Global Financial Crisis over inflation concerns, yet currently advocates for greater policy easing driven by a view that productivity gains could boost growth without driving inflation. This intellectual framework aligns with the Trump administration’s preference for lower rates, but represents a potential pivot from Powell’s more data-dependent approach.

Analysts warn that unless private investors rush en masse to absorb Treasury securities that the Fed would sell, an abrupt reduction of the central bank’s balance sheet would push up long-term interest rates, running counter to ambitions to see mortgage rates fall.

Precious Metals Defy Geopolitical Logic; Gold Tumbles

Gold has experienced counterintuitive price action during the crisis, falling 4.38% on March 4 despite traditional safe-haven expectations. By March 5–6, gold traded near $5,066, losing all intraday gains as investors favored U.S. Dollar safety over traditional precious metals.

Technical analysts have identified concerning bearish formations, with gold forming a double top at recent highs, signaling potential downside pressure. Critical support at $5,100 represents the key pivot, with a break below triggering potential retests of mid-February lows around $4,844.

The unexpected selloff reflects several dynamics: investor relief that U.S. military capabilities appear sufficient to prevent protracted conflict, continued strength in U.S. economic data, and profit-taking after extended rally runs.

Oil Price Scenarios and Inflation Implications

Energy analysts present a wide range of crude oil price scenarios depending on the duration and severity of supply disruptions. Goldman Sachs has calculated an $18 per barrel live risk premium, with suggestions that this premium would moderate to $4 per barrel if only 50% of Hormuz flows halt for a month.

More pessimistically, if the blockade persists for more than three weeks, Brent crude will likely breach the $100 per barrel mark. Barclays has raised its Brent crude forecast to $100 per barrel, while Morgan Stanley analysts warn that Iranian actions could cut global supplies by up to 3 million barrels per day.

These price trajectories carry profound implications for inflation expectations. Before the conflict, global inflation was projected at 3.8% for 2026; current estimates now suggest potential for spikes above 4.5% if the Strait remains blocked. This creates a policy dilemma for the Federal Reserve, which faces pressure to support labor markets through rate cuts while being constrained by upside inflation pressures from energy.

What Traders Must Watch

Friday’s nonfarm payrolls data will prove the critical pivot point for near-term forex market direction. Three scenarios present dramatically different implications:

- “Goldilocks” scenario (70K–90K jobs): Equities would likely cheer moderate weakness as justifying future easing, supporting the dollar through delayed rate-cut expectations.

- “Stagflation” shock (low jobs, high wages): The Fed would face a policy trap, unable to cut rates due to inflation pressures, weighing heavily on the dollar.

- “Recession” scenario (near-zero or negative jobs): Flight from equities into bonds and gold would trigger substantial dollar weakness.

Technical levels to monitor include EUR/USD support at 1.1578, GBP/USD support at 1.3340, and AUD/USD consolidation between 0.7000–0.7150. For oil, sustained breaks above $85 per barrel would extend inflation concerns and constrain Fed easing.

Market Impact Analysis

The intersection of geopolitical disruption, energy supply shocks, labor market uncertainty, and central bank policy transitions creates an extraordinarily complex trading environment. The U.S. Dollar’s near-term strength appears supported by safe-haven flows and repriced rate-cut expectations, yet FX strategists remain skeptical that this strength will persist given longer-term structural factors supporting dollar weakness.

The Strait of Hormuz closure represents a genuine supply shock to global energy markets with credible scenarios suggesting $100+ crude if disruptions persist beyond three weeks. This energy premium will likely suppress emerging market currency performance while supporting energy-exporting nations—a dynamic that will require careful currency pair selection for traders seeking to capitalize on volatility.

Alexandra Winters says:

“The dollar’s current strength rests on a fragile foundation of short-covering and repriced rate-cut expectations, not genuine safe-haven demand—a distinction that matters critically when crude disruptions threaten to accelerate inflation at precisely the moment the Fed faces mounting pressure to ease. Traders should prepare for substantial directional whipsaw on Friday’s payrolls, as a disappointing number could shatter the Fed easing-delay narrative and trigger sharp dollar weakness, while any surprise strength would cement near-term greenback dominance despite longer-term structural headwinds.”